When it comes to rural property transactions, Brad Sewell from Robinson Sewell Partners hasn’t witnessed many finance issues in the current cycle.

“The process has certainly improved in recent years, and the required time-frames are being articulated more clearly to both purchasers and vendors,” he said.

Brad Sewell

Mr Sewell is currently settling a property in western Queensland, which he described as ‘standard.’

“It was an expressions of interest process and an offer was lodged with a 28-day finance clause. Finance was approved 48 hours later than anticipated, but the property settles this week.”

He explained that it was acceptable for properties listed for private treaty or expressions of interest to receive an offer ‘subject to finance’.

“This is proposed by buyers who don’t want to go through the expense and time of obtaining finance unless their offer is accepted.”

Conversely, buyers must turn up to an auction finance-ready, because they need to pay a deposit.

Mr Sewell said vendors and their solicitors are generally happy to accept finance clauses.

“Previously, there was a push-back, but it is mainstream now. A finance clause is typically 28 days or four weeks giving banks or financial institutions sufficient time to get an approval in place, subject to a valuation.”

Two years ago, Mr Sewell raised concerns that some agents were setting unrealistic expectations on the other parties to complete. However, he said the turnaround time was sometimes impacted by a complex deal or by under resourced banks, accountants and solicitors.

At the time, Queensland had introduced new measures which Mr Sewell believed would take pressure off the parties involved in a property transaction.

“Finance clauses allow purchasers to sign a contract on a property, pay a deposit and are then given 21 to 28 days to get their finances sorted, upon which the contract becomes binding.”

He said the process involved in transacting rural properties has certainly improved.

“Back then, there was still risk aversion as banks remained cautious following the severe drought from 2017 to 2020. Today, there’s a cracker of a season, particularly for grain growers, in northern New South Wales and Queensland.”

Mr Sewell said changes include:

Agents’ educating vendors – there were a number of years where the timing was out, on everything. Today, agents adjust a vendor’s position so it runs more realistically. In other words, they are balancing getting the vendor’s ducks lined-up, and completing a sale.

Banks are quicker in making a decision compared to previous years, banks currently have more confidence in agriculture and their finance decision making systems are quicker.

Sales processes have improved – in the past, some finance offers were subject to 14 days and that was never enough. Today, 28 days allows banks ample time to obtain relevant information from the purchaser, assess the deal, get it through credit and action it.

Expressions of interest process

Recently, Mr Sewell has witnessed a big uplift in expressions of interest campaigns in rural property sales.

In the last four months, he has been involved in three property sales around the Charleville district – all under expressions of interest.

Mr Sewell admitted EOIs were ‘not much fun’ for a purchaser.

“A successful buyer has no idea how much more they paid than the next person and that can lead some purchasers to question how much of a premium they paid.”

His partner Ian Robinson said the banks are carrying out more due diligence, which is a good process to have in any business.

“That due diligence means more detailed information needs to be provided by the borrowers to the banks to satisfy credit and technical criteria. In short, many delays are caused by borrowers not being ‘presentation ready’ to the banks and the banks are wearing the frustration or the blame.”

If producers are in the mindset of looking to buy, then Mr Robinson urged them to get themselves ‘presentation ready.’

“There is quite a lot of work involved, but that carries forward. So when a producer finds a property they want to purchase, they are 75 percent ready. All they need to do is dovetail the technical information of that particular acquisition and their data pack is ready for the bank.”

He said waiting to find the right property and starting from ground zero means they will be a long way behind the game.

“Especially if there are other borrowers out there who are presentation ready and have their cash pre-approved – there’s a good chance they will be missing out on the opportunity.”

Tim Ferrier, Sparke Helmore Lawyers

Tim Ferrier, a consultant lawyer specialising in agribusiness at Sparke Helmore Lawyers, said banks are undertaking greater prudential assessments for rural property sales.

Tim Ferrier

“Typically, banks are taking at least 30 days to finance or release funds ready for settlement,” he said.

As a result, banks lacked nimbleness and agents were adjusting their processes.

“Most selling agents are realistic in factoring in finance approval times in marketing campaigns and are advising their clients accordingly,” Mr Ferrier said.

He said when it came to approving loans, the banks considered each application on a case-by-case basis.

“Once a bank has received a valuation, it assesses the report, considers any concerns and decides whether to proceed. As a result, an interested party should allow for at least 30 days.”

Mr Ferrier said there were many legal issues involved in transacting rural assets, which meant the process in buying or selling rural property can vary greatly from one sale to another.

“Due to the size of land and number of assets that go with a rural sale, it is important to ensure a buyer or seller has considered all risks and factors before entering into anything that is legally binding.”

Mr Ferrier said property valuations also took time.

“A seller needs to consider what level of valuation the bank or the financier requires. Assessments don’t happen with a click of the fingers. There is no such thing as a desktop valuation – a property needs to be physically examined.”

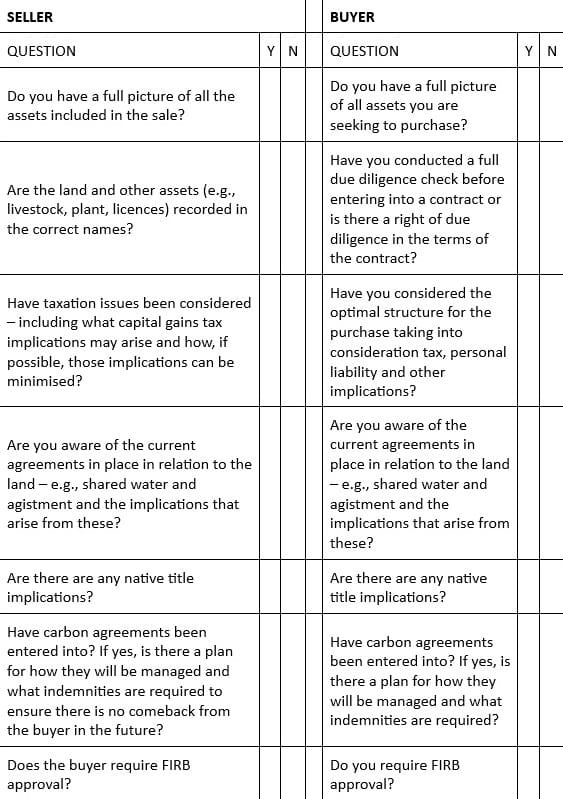

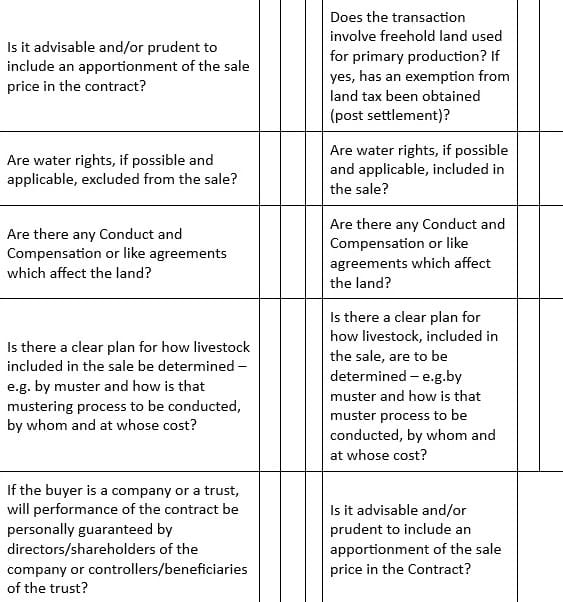

Mr Ferrier has prepared a list of top tips to prepare for the sale or purchase of rural property.

“Good preparation increases chances of success, reduces risks and ensures informed decisions can be made about the sale or purchase,” he said.

HAVE YOUR SAY