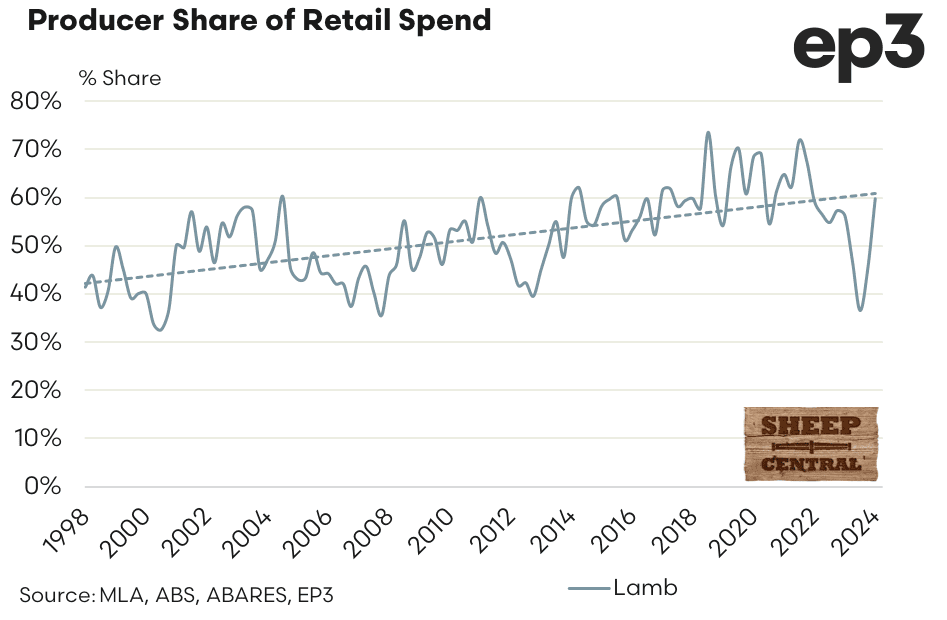

AUSTRALIAN lamb producers’ share of the retail dollar spend for their product has edged higher in the March quarter, after hitting near-record lows in December.

Friday’s release of March quarterly Consumer Price Index data from the Australian Bureau of Statistics provides the opportunity to update the quarterly producer share of retail dollar calculation published jointly by Episode3 and Beef Central.

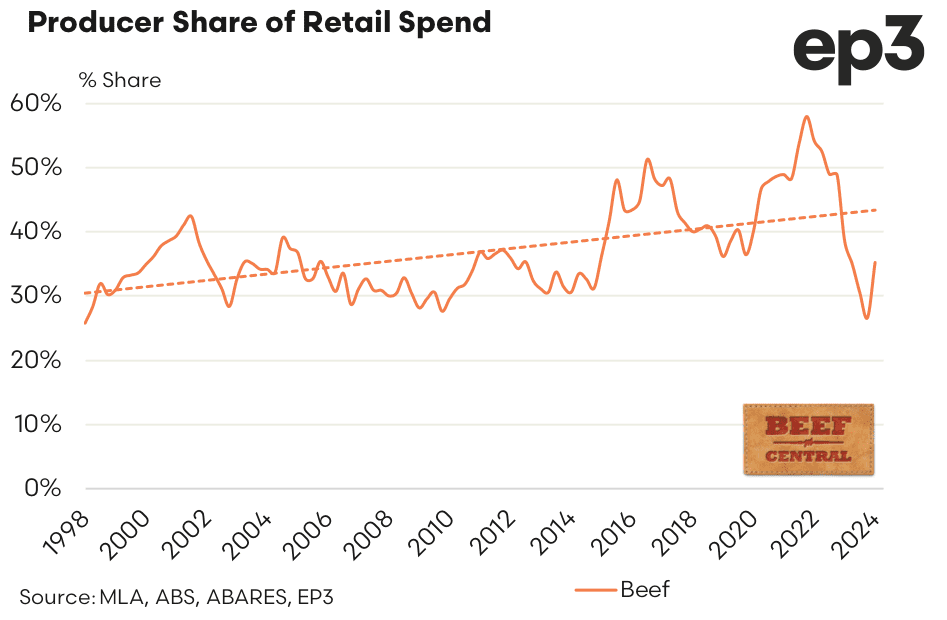

As can be seen on the graph above, the steady decline in saleyard cattle prices during the fourth quarter of 2023, combined with a marginal easing of retail beef prices, saw the beef producer share of retail $ in December drop to its lowest point since the data-set began back in 1998, at just 25.8 percent.

Since then, the share value has lifted to a little over 35pc in the March quarter. This is the best result seen for producer share since the second quarter of 2023, but a long way off the long-term trend line growth seen since the late 1990s.

Back in 2022-23 when cattle prices approached record levels, the producer share index soared to almost 60pc.

Improving livestock prices during the first quarter have seen both beef and sheepmeat producers (sheepmeat results below) capture a greater share of the retail spend as CPI data for average retail beef and lamb pricing shows at the consumer end the price for meat has continued to ease. However, the additional share being retained by beef versus sheep producers isn’t being equally distributed, Ep3’s analysis found.

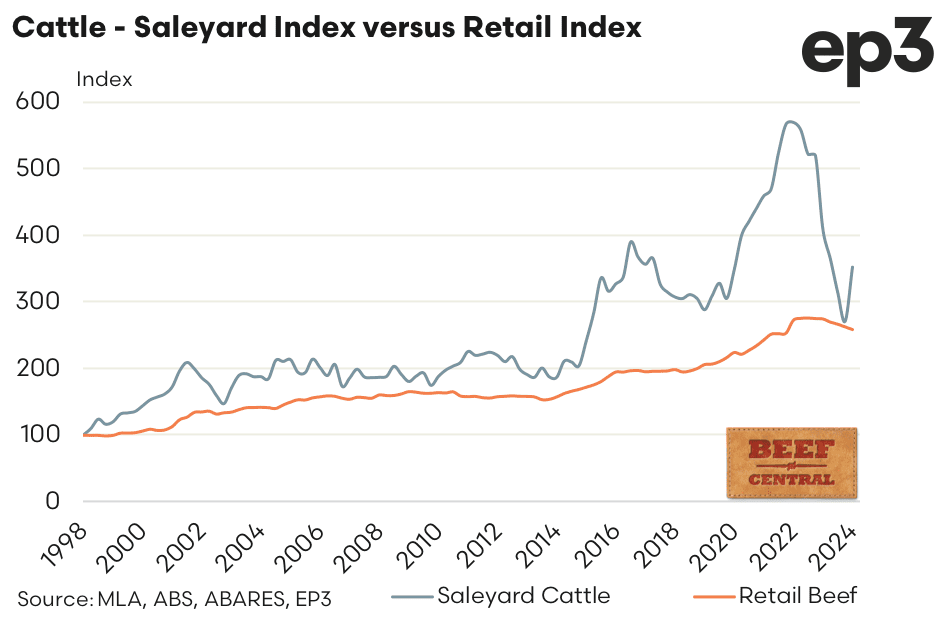

In the graph above comparing the saleyards cattle price index versus the retail price index (1998 providing the benchmark at 100 for both), the saleyard index lifted 30pc over the March quarter 2024, from 271 to 352. As was the case with sheepmeat at the retail level, the retail beef prices eased marginally over the first quarter of 2024, with the CPI data showing a decline of 1.5pc with the retail index dropping from 262 to 258.

As was the case with retail pricing being slow to respond to falling livestock prices seen during the end of 2023, there is also a lag effect when livestock prices rebound.

Lamb result shows improvement

A similar quarterly retail share calculation is made for lamb producers.

Improving livestock prices during the first quarter of 2024 have seen sheep producers capture a greater share of the retail spend as CPI data for average retail lamb pricing shows at the consumer end the price for meat has continued to ease.

In terms of the producer share of the retail spend (see graph below), the lamb sector has seen a solid recovery over the last quarter with the proportion rising from 45pc in the December quarter to almost 60pc at the end of March. This is the highest the producer share seen for sheep farmers since the first quarter of 2022, and places the producer share back in line with the trend line growth seen since 1998, as outlined by the dotted trend line.

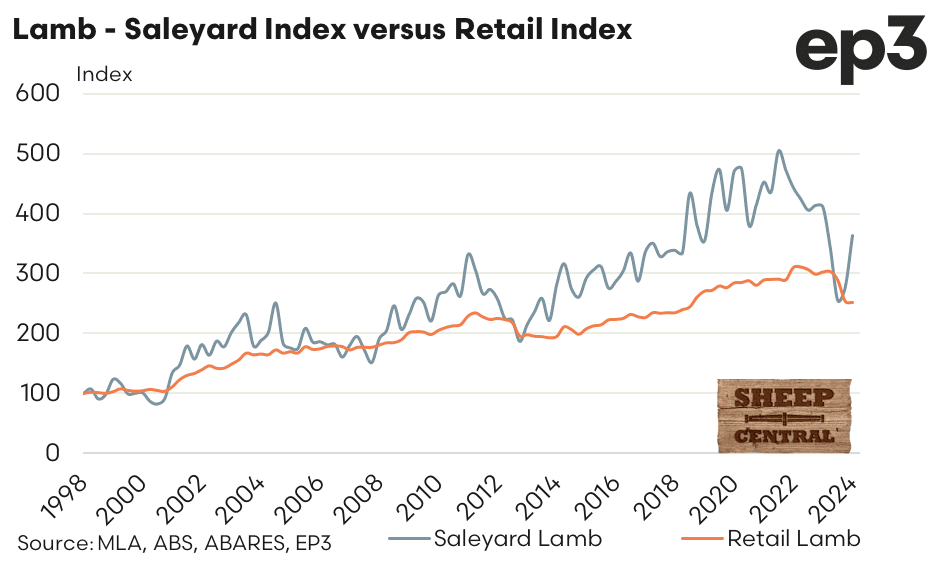

According to the saleyard index versus retail index, saleyard lamb pricing saw a 31pc increase from the end of 2023 to the end of March 2024, from 276 to 363. However, over the first quarter of 2024 retail lamb pricing hardly moved, with the index easing marginally from 254 to 252, a fall of less than 0.1pc.

Background to the producer share of retail prices calculation

In collaboration with analyst Matt Dalgleish from Episode 3, Beef Central in July last year launched a new quarterly series looking at trends in the beef producer’s typical share of the retail consumer’s spend on beef products.

A similar analysis was compiled by MLA for four years, before being discontinued by the industry service delivery company back in December 2016. The project was originally launched as a result of producer requests during the 2012 MLA annual general meeting.

A similar analysis was compiled by MLA for four years, before being discontinued by the industry service delivery company back in December 2016. The project was originally launched as a result of producer requests during the 2012 MLA annual general meeting.

Beef Central sought, and gained MLA’s blessing to resurrect the discontinued series, based on clear reader interest. The same formula is used to compile the new set of results as originally used by MLA (see explanation at base of page).

Episode 3 and Beef Central now jointly publish a quarterly report, soon after ABS quarterly retail beef price data is released. This typically happens in late July, late October, late January and early May.

The exercise sees national saleyard cattle prices in carcase weight terms being converted into an estimated retail weight equivalent and compared to average retail beef prices, as reported by ABS (see summary below).

About the producer share of retail spend calculation

The beef producer share of the retail dollar is calculated using a range of assumptions:

- The national saleyard trade steer indicator is used as the benchmark livestock prices, representing animals suited for the domestic market. Livestock prices are collected by MLA’s NLRS.

- Converting the carcase weight price to an estimated retail weight equivalent price is achieved using a retail meat yield for beef of 68.7pc.

- The indicative retail meat prices are calculated by indexing forward actual average beef prices during each quarter, based on meat sub-group indices of the Consumer Price Index, provided by ABS. These indices are based on average retail prices of selected cuts (weighted by expenditure) in state capitals.

The producer share is calculated by dividing the estimated retail weight equivalent livestock price by the indicative retail price.

Click here to read earlier reports in this series:

Should cattle producers be paying more attention to retail margin share?

Beef Central’s project partner Episode 3 is an independent, data-driven market analysis service providing insights and reports to the agriculture industry, food manufacturing sector and their associated markets. Through robust analytical assessment, EP3 assists agricultural stakeholders to make better, more informed decisions that drive profitability. The company is experienced in producing high-quality reports used by government, RDC’s and corporate entities. In addition, EP3 is available on a retained basis with clients to provide on-going and bespoke information to assist in their sales or purchasing process. Click here to access the Episode 3 website.

Beef Central’s project partner Episode 3 is an independent, data-driven market analysis service providing insights and reports to the agriculture industry, food manufacturing sector and their associated markets. Through robust analytical assessment, EP3 assists agricultural stakeholders to make better, more informed decisions that drive profitability. The company is experienced in producing high-quality reports used by government, RDC’s and corporate entities. In addition, EP3 is available on a retained basis with clients to provide on-going and bespoke information to assist in their sales or purchasing process. Click here to access the Episode 3 website.

Farmers’ share of the consumer dollar has always been an absurd measure of marketing efficiency, and is now even worse given that most meat sold on the domestic market is sold by supermarkets. Supermarkets have even greater capacity to adjust margins to smooth consumer prices than traditional butchers. In any case, export prices are the main determinant of prices received by farmers.

Yet again Dr Alastair Watson washes aside the smoke and mirrors and succinctly reveals an economic reality.