INCREASES in wool, lamb, beef, live cattle and dairy export earnings are forecast to keep Australia’s gross value of farm production above average next financial year.

INCREASES in wool, lamb, beef, live cattle and dairy export earnings are forecast to keep Australia’s gross value of farm production above average next financial year.

The gross value of farm production in 2017-18 is slated to be 9 percent higher than the average of $55 billion over the five years to 2016-17, the Australian Bureau of Agricultural and Resource Economics and Sciences said in its June Agricultural Commodities report.

The ABARES report said expected declines in export earnings from mutton, wheat, sugar, coarse grains, canola, chick peas meant the gross value of Australian farm production is forecast to dip by 4.6pc to $59.9 billion in 2017-18.

Click here to get the latest Sheep Central story links sent to your email inbox.

Saleyard lamb prices expected to lift 5pc

In 2016-17, ABARES is expecting Australian saleyard prices for lambs to average of 595c/kg, up 12 per cent from 2015-16. In 2017-18, lamb prices are forecast to rise by a further 5pc to average 625c/kg, reflecting continued, albeit slower, flock rebuilding and growing demand for lamb in Australia’s key export markets. ABARES said the forecast higher prices reflect strong demand for restocking as graziers rebuild their flocks in response to improved seasonal conditions in 2016 and 2017.

ABARES expects lamb slaughter to fall by 3pc to 22.5 million head in 2016-17, representing a 2pc drop in production to 506,000 tonnes as higher average carcase weights compensate for the reduced turn-off. In 2017-18, lamb slaughter is forecast to increase by 1pc to 22.8 million head, reflecting higher sheep numbers in the national flock. Lamb production in 2017-18 is forecast to increase by 2pc to 516,000 tonnes.

In 2017-18, the volume of lamb exports is forecast to increase by 2pc to about 261,000 tonnes as lamb production increases. Lamb export earnings are forecast to rise by 4pc to $1.94 billion for the year.

New Zealand lamb production is forecast to fall by 1pc to 288,000 tonnes in 2017-18, potentially supporting increased demand for Australian lamb in key export markets.

Mutton prices to increase in 2017-18

Sheep prices are estimated by ABARES to have increased by 33pc to a weighted average of 420c/kg in 2016-17, compared with the previous year, reflecting increased retention of breeding ewes to rebuild flock numbers. In 2017-18, sheep prices are forecast to increase by a further 4pc to average 435c/kg over the year. This reflects an expected continuation of flock rebuilding, assuming average seasonal conditions, ABARES said.

Sheep slaughter is estimated to finish 18pc lower in 2016-17 at 6.7 million head, reflecting greater retention of sheep for breeding, with the mutton production forecast down 17pc to about 163,000 tonnes. In 2017–18, sheep slaughter and mutton production are forecast by ABARES to fall as flock rebuilding continues. In 2017-18, mutton exports are forecast to fall by a further 6pc to about 121,000 tonnes as graziers continue to retain breeding ewes for flock expansion.

ABARES forecast live sheep exports in 2017-18 to grow by 1pc to about 1.9 million head, driven by strengthening Middle East demand, although continued flock rebuilding is expected to limit growth in live exports.

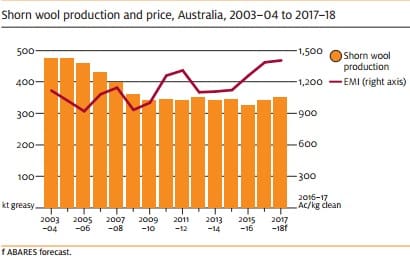

Wool price support from export demand

In 2017–18, the AWEX Eastern Market Indicator for wool prices is forecast to rise by a further 3pc to average 1445c/kg clean, supported by forecast growth in export demand for wool. Strengthening economic growth in the United States and growing consumer demand in China are expected to drive increased demand for apparel wool, particularly in the finer micron range, ABARES said.

Australian wool exports are forecast to increase by 3 per cent to 442,000 tonnes in 2017-18, as the number of sheep available for shearing continues to grow. ABARES is forecasting the value of wool exports to increase by 6pc to $3.9 billion for the year. In 2017-18 wool exports to China are forecast to increase by 3pc to 343,000 tonnes and account for 78pc of total Australian exports.

In 2016-17 higher wool prices have led to a reduction in the price-competitiveness of wool against alternative fibres in $US dollar terms, ABARES said. In the 10 months to April 2017, the price of 21-micron wool increased by 4pc compared with the price of polyester staple fibre and by 7pc against the price of cotton. This suggested that polyester and cotton will be substituted for wool in the short term, particularly in the manufacture of budget clothing. However, ABARES said the wool content of luxury and some sporting apparel is less likely to be affected because wool remains the preferred fibre in these niche markets. Consumer demand for woollen apparel is forecast to gradually recover in 2017 after consumption fell in 2016.

ABARES expected graziers to continue to expand their sheep flocks in 2017–18. The bureau said a continuing trend towards meat breeds and dual-purpose sheep — which tend to have higher twinning rates — is expected to drive higher lamb markings. As a result, the national flock is forecast to rise by a further 4pc to around 76.6 million head by the end of June 2018.

Beef and wool lead export earning forecast

Acting ABARES executive director, Peter Gooday, said despite the forecast decline in overall export earnings, the outlook for this year was positive, up almost $5 billion compared with the five year average.

“The gross value of livestock production is forecast to increase by 3.5pc to $30.2 billion in 2017-18, driven by forecast increases in prices for livestock products, particularly wool and dairy.

“Export earnings from farm commodities are forecast to remain relatively unchanged at $48 billion in 2017-18,” Mr Gooday said.

The agricultural commodities for which export earnings are forecast to rise in 2017–18 are beef and veal (up 4pc), wool (6pc), dairy products (14pc), cotton (34pc), wine (5pc), lamb (4pc), live feeder/slaughter cattle (3pc) and rock lobster (2pc).

The forecast increase in export earnings in 2017-18 is expected to be partly offset by expected declines for wheat (down 3pc), sugar (7pc), coarse grains (23pc), canola (19pc), chickpeas (44pc) and mutton (5pc).

Mr Gooday said export earnings for fisheries products were forecast to increase by 1.2pc in 2017-18 to $1.5 billion.

“In Australian dollar terms, export prices of wool, wine, lamb, barley, cheese and mutton are forecast to increase in 2017-18.

“Export prices for beef and veal, sugar, canola, live feeder/slaughter cattle, chickpeas and rock lobster are forecast to fall, with export prices for wheat and cotton forecast to remain relatively unchanged,” Mr Gooday said

The June quarter issue also features an article on China’s grain policies, and information on seasonal conditions in Australia and chilled beef exports to China.

The Agricultural Commodities, June quarter 2017 issue is available at ABARES Publications.

Click here for the the ABARES lamb saleyard price and slaughter 2003-2018 graph.

{kind=link}

Click here for the ABARES sheep saleyard price and slaughter 2003-2018 graph.

{kind=link}

Click here for the ABARES shorn wool production and price 2003-2018 graph.

{kind=link}

HAVE YOUR SAY