The battle for Australia’s land use is heating up with cropping, livestock production, forestry, conservation and government needs all competing for the same land, independent meat and livestock analyst Simon Quilty from Global Agritrends suggests in a recent paper.

Simon Quilty

The extreme drought of 2018 and 2019 profoundly impacted land use in marginal farming areas of Australia and has made many farmers rethink how they manage the next drought, he suggested.

“As a result, there have been significant changes in livestock numbers and cropping across many regions and states. Recent data released from the Australian Bureau of Statistics on Australia’s slaughtering’s and herd and flock size, when added to these land use changes, all point to some unexpected changes in how farming land will be used over the next 20 years,” Mr Quilty said

His paper also explores the likely impact on rebuilding livestock numbers in each state.

Five surprising trends have evolved in the livestock sector:

- A slower growth rate in the Australian cattle herd, even though there have been two years of record cattle prices

- Ongoing liquidation of the Australian dairy herd, even with record milk prices

- A significant increase in cropping across many states

- The expansion of forestry and conservation land, and

- The migration of the Australian sheep flock onto the eastern seaboard where it is expanding at a much higher rate than cattle.

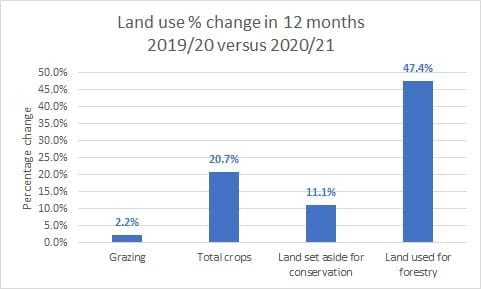

Land use is changing quickly

Australia’s land use measured annually from June 2020 to June 2021 has seen dramatic shifts towards forestation, cropping and conservation, the papers shows.

Land for forestry saw the most significant percentage shift with 47.4pc increase over 12 months, followed by cropping at 20.7pc, conservation at 11.1pc, and grazing at a mild 2.2pc increase.

These land use changes reflected government policy, private sector investment and the degree of risk the farming community perceives and the need for change, Mr Quilty said.

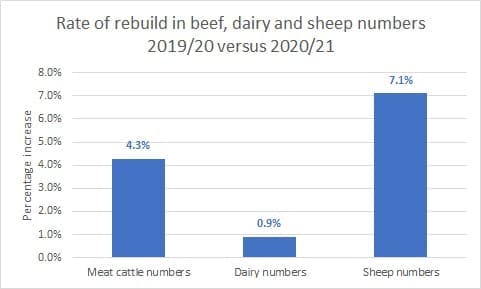

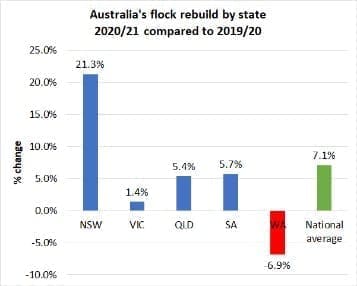

The increase in grazing by 2.2pc needed closer attention, as the actual rebuild has been more in sheep and lamb numbers at a national average of 7.1pc, compared to the herd growth for beef cattle at 4.3pc and 0.9pc for dairy.

“This focus on sheep versus cattle is surprising for some, given record cattle and dairy milk prices in the last two years. Cropping has also played an essential role in displacing livestock, potentially putting a brake on livestock numbers in certain states in Australia,” he said.

The slow rebuild in cattle (both beef and dairy) and the shift into cropping and sheep highlighted significant ongoing changes likely in the livestock industry’s makeup over the next ten years and beyond.

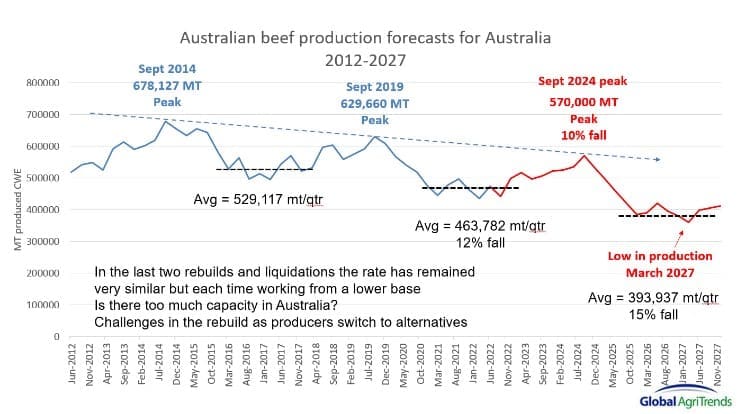

Cattle herd expands at a slower pace, from a much lower base

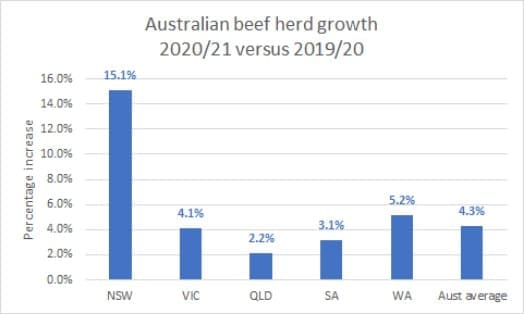

The Australian beef herd increased by only 4.3pc in 2020/21. The national figure masks the fact that NSW grew three times the national average at 15.1pc, and QLD growth fell to almost half the national average at 2.2pc for the year.

So there was a natural flow of livestock from QLD into NSW, which saw NSW ‘beg, borrow and steal’ from QLD as it attempted to rebuild to make up for the extreme losses of the 2018/19 drought, Mr Quilty said.

“It should be noted that the national cattle herd rebuild is starting from a much lower production base. As a result, beef production volumes will likely struggle to reach significant volumes before the next liquidation cycle begins. This is on the assumption of a 2.5-year rebuild period, which is what the last two rebuild cycles have done, followed by a dry period. In short, Australia’s rebuild is starting from a low base and is likely to run out of time to rebuild significant numbers before the next drought occurs,” he said.

The shift to alternate enterprises would see limited national cattle expansion, namely cropping and sheep production that will be switched to, he said.

The shift to alternate enterprises would see limited national cattle expansion, namely cropping and sheep production that will be switched to, he said.

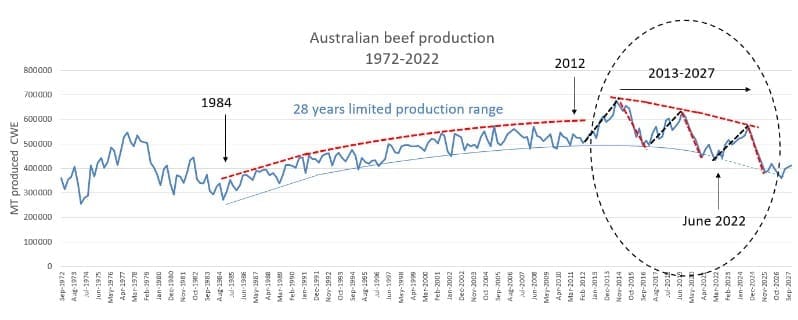

“I am forecasting the next peak in production to occur in September 2024. This would be exactly five years since the previous peak in September 2019, which was also five years since its previous production in September 2014.

“Each production peak is a step lower than the previous, with a 10pc expected fall in beef production for September 2024 compared to September 2019. Nonetheless, this is when Australia’s beef supplies will be most abundant,” he said.

In an ideal world for Australian meat processors, this was when global meat prices will be firm, given the severity of the current US drought, which will coincide with cheaper Australian cattle prices and strong global beef demand – meaning Australian processor packing margins are likely to be good when this occurs.

Mr Quilty’s next forecast low in Australian beef production is more concerning, likely to be between 2026 and 2027, with production expected to be 15pc lower (394,000t per quarter) than the current quarterly average low of the last two years (464,000t per quarter).

“This is based on the belief that the Australian herd liquidation rate will be similar to the last two liquidation periods. The ramifications of such a low beef production base will have consequences for Australian meat processors, restockers, labour requirements, export markets, product type, etc,” he said

Shift from beef to cropping and sheep

The switch to sheep and cropping was occurring across many states, with forestry and land conservation being part of the change in land use, Mr Quilty said.

“The net result is less grazing land for cattle.”

Exclusion fencing, designed to keep pests from grazing land such as wild dogs, feral rabbits, pigs, goats and cats has played an essential role in helping to manage marginal grazing areas, making it more attractive for sheep.

In the last five years, thousands of kilometres of exclusion fencing have been erected in western NSW and western QLD. Before the drought, cattle had been predominately in these areas. Since the extreme drought conditions of 2019, cattle have been replaced by sheep and goats, which are more suitable for these marginal regions and easier to feed in droughts.

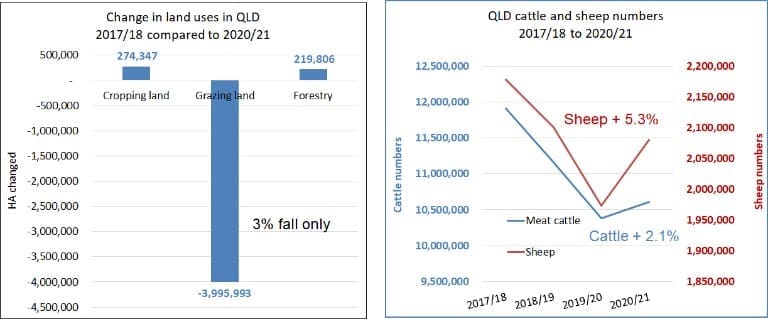

QLD: change in enterprises

QLD is Australia’s largest cattle-producing state with close to 10.6 million head of cattle, or 48pc of the national herd, according to ABS data.

During the 2020/21 year, the state’s sheep numbers rose 5.3pc, while cattle numbers increased by only 2.1pc.

“Two things happened during that year, firstly, marginal land in western QLD moved into sheep and goat production, and secondly, as stated earlier, NSW bought significant cattle numbers out of QLD to try to restock quickly. The bottom line has seen subdued herd growth in QLD,” Mr Quilty said.

There was also a significant reduction in grazing land of four million hectares – the state government having taken back land for military and conservation purposes. In addition, indigenous groups and conservation organisations have also acquired significant land holdings. This land was being destocked in each instance and was unlikely to be used for grazing again, Mr Quilty said.

There was also a significant reduction in grazing land of four million hectares – the state government having taken back land for military and conservation purposes. In addition, indigenous groups and conservation organisations have also acquired significant land holdings. This land was being destocked in each instance and was unlikely to be used for grazing again, Mr Quilty said.

Another less significant impact has been the increase in forestry and cropping land.

“In each instance, it points to a slower herd rebuild over the next two years, and with the likelihood of drier conditions/drought not far away – the ability for QLD to rebuild any significant numbers in a short period is unlikely,” he said.

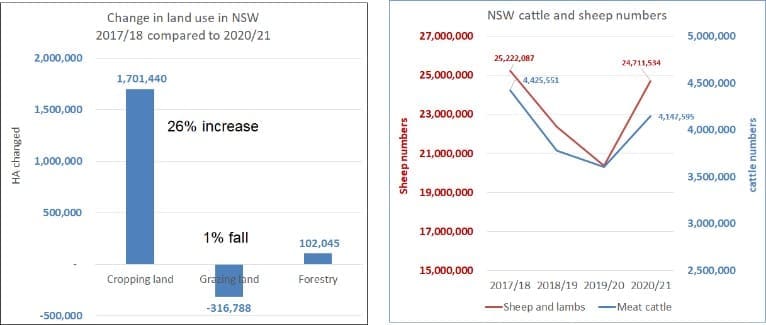

NSW: change in enterprises

The changes in NSW beef herd were different to QLD and VIC, with cropping playing a much more significant role and the importance of extensive restocking from WA seen in 2020 and 2021.

“The NSW beef herd has still not regained its original herd size since the pre-drought years, being 6pc lower in size, whereas the sheep flock is only 2pc lower and looks to be on track to surpass the 2017/18 numbers this year,” he said.

The ability to buy cattle and sheep from other states was limited (supply has been exhausted). Nonetheless, marginal land was being made available to smallstock (sheep and goats).

Cropping in NSW is 26pc higher over the last three years and is more likely to have displaced cattle than sheep, and the data shows an overall fall of 1pc in grazing land.

“The competition for differing land use in NSW is alive and well,” Mr Quilty said.

“The NSW cattle herd rebuild is still underway, but the momentum of 15.1pc growth is unsustainable, and growth is likely to slow to an average rebuild pace of 4pc or less, which if true, still puts the herd size below pre-drought levels.”

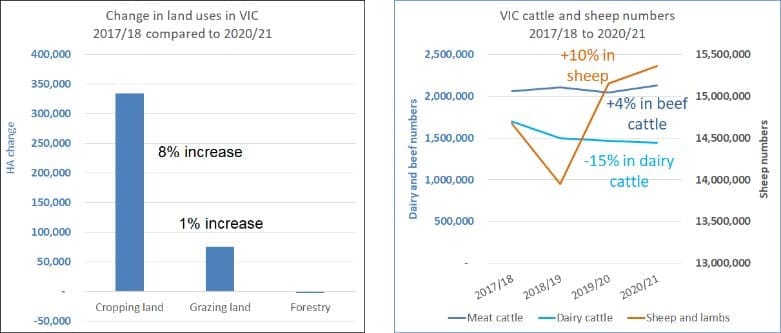

VIC: change in enterprises

VIC has had one of the most significant state increases in flock size, with a 10pc increase in the last two years compared to cattle, with only a 4pc increase. Cropping has also increased dramatically by 8pc over three years at the expense of grazing, particularly cattle.

The surprising ongoing herd decline is the VIC dairy sector which has fallen 15pc in four years, and the current female kill ratio in Victoria points to continued liquidation in the current year. This is despite record dairy prices with milk solids at $9 to $10/kg.

“I was told that 30 dairy enterprises left the VIC dairy industry last year. The reasons given are the age of the average dairy farmer exiting the industry, the lack of willingness by younger generations to take over the business and the difficulty in finding labour. An additional 30 enterprises are expected to leave in the next 12 months – so expect ongoing liquidation,” Mr Quilty said.

What is also surprising is the number of dairy operations switching to sheep production in preference to beef – the ABS figures would support this anecdotal trend.”

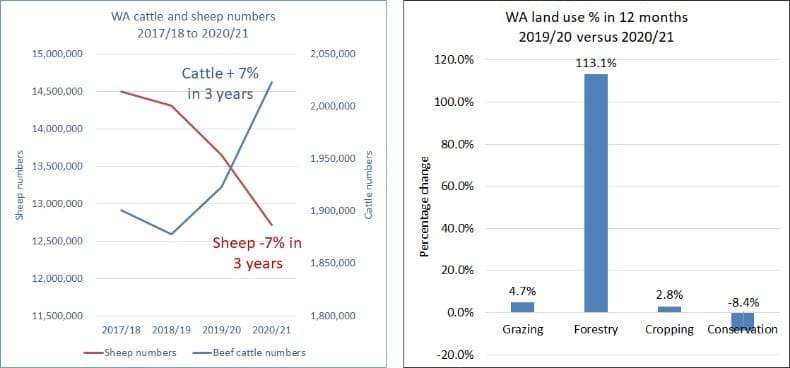

WA: change in enterprises – bucking the trend –

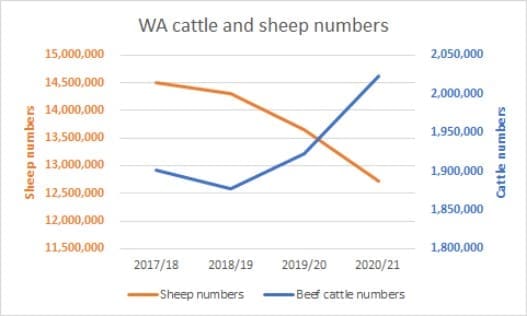

WA has bucked the trend across Australia with declining sheep numbers and beef cattle operations rising. This is no surprise given that live sheep exports have declined for the last four years, with moratoriums being placed on shipments over several months in the middle of each year.

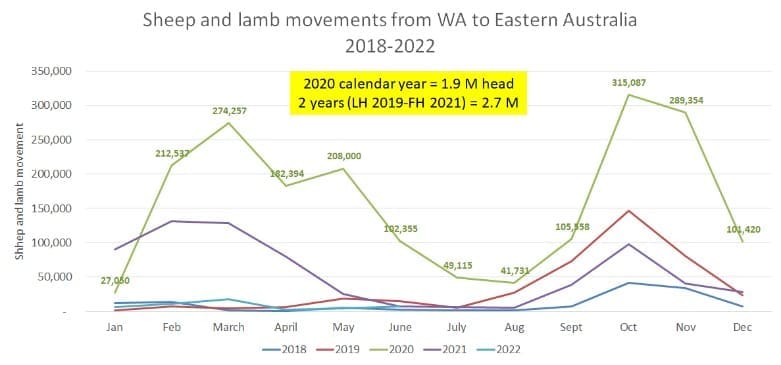

In addition, the two-year movement of sheep and lambs from WA to the Eastern Seaboard in late 2019, 2020 and early 2021 saw 2.7 million head move across. This was important in helping NSW and other eastern states restock over that period.

“The movement into forestry and, to a lesser extent, cropping has also been significant,” Mr Quilty said. “Sheep numbers still dominate the WA livestock sector by more than a 6:1 ratio compared to cattle, but the trend of lower sheep numbers is likely to continue.”

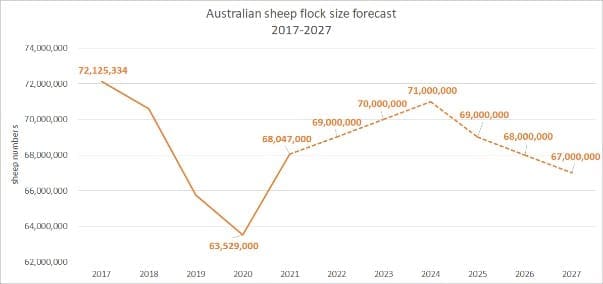

Australia’s flock rebuild is moving higher

Australia’s flock rebuild has migrated to the Eastern Seaboard and would move higher over the next ten years as sheep numbers increase across marginal areas of NSW and QLD, Mr Quilty said.

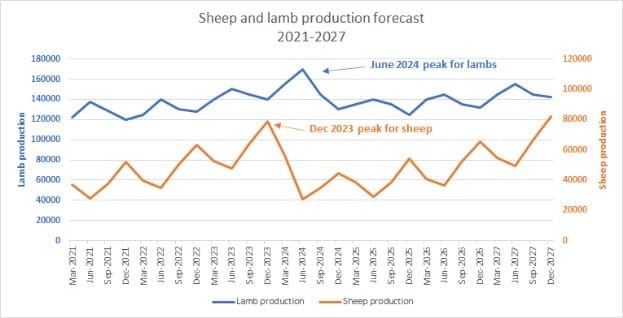

The move in recent years into sheep farming in preference to cattle points to a healthy increase in the flock that will see the next sheepmeat production peak in 2024 at close to 4pc above the last peak, he said.

Anecdotal evidence pointed to ongoing liquidation in WA as the decline since 2017/18 of 12pc was likely to continue. The combination of the ongoing embargo on live sheep exports, the threat of FMD, the flexibility of cropping, and the high cattle prices (and less labour required) all contributed to the liquidation of the WA flock.

The size of the Australian flock is expected to expand to 71 million, well short of the original forecast of 75 million. This peak is expected in 2024. In 2013 the flock was at 75.5m head. Given the pressure on land use, it was unlikely that Australia would regrow the flock to these once high levels of production ever again, he said.

Key trends that will re-emerge in the future

Key trends that will re-emerge in the future

The following key trends are expected to emerge, Mr Quilty’s paper said:

The Australian beef herd rebuild rate is slowing, which will see a step down in beef production levels in the next five-year cattle cycle.

- Ongoing liquidation of the dairy industry is expected.

- The peak beef production highs are expected to be lower, and the low periods of production (2026-27) are expected to be even lower (15pc) than today.

- The flock is migrating from the west to the Eastern Seaboard. Ongoing flock liquidation in the west is expected, and a gradual flock increase in the east will continue.

- Land use is changing quickly due to the extreme drought of 2018 and 2019. Cropping, forestation and land conservation are on the increase in most states.

- Restockers will play their role again in the production low of 2026-27 with fewer cattle and more grass. Expect new record cattle prices.

- Processing capacity will be an issue with potentially excess beef capacity and not enough small stock capacity on the Eastern Seaboard – dual species operations will have a comparative advantage.

Fewer cattle available to process will see the need for more value-adding through feedlots. Feedlot capacity may expand slightly but will increase as a percentage of exports with lower production expected.

Conclusion

Risks for cattle and sheep producers are defined in many ways, including price risk, input risks, disease risks etc. and drought risk.

The underlying influence on many of the land use changes outlined in his paper was drought risk, Mr Quilty said.

“In the past, farmers have made provision for drought by buying extra feed, destocking and ensuring enough water is available, but this data tells me that the decision by farmers to move away from cattle in certain regions is about how sustainable these areas are for cattle in severe droughts, such as the marginal regions of western QLD and western NSW, where sheep and goats have displaced cattle which are more suited to these areas in drought – this to me is a long-term structural change,” he said.

The displacement of grazing land by the government, forestry, indigenous groups and conservation organisations pointed to strong demand from other sectors for limited grazing land that is unlikely to return to grazing – once again a long-term structural change.

US drought impact

While both Australia’s cattle herd and sheep flock are likely to rebuild and liquidate over the next five years, at the same time the US herd will desperately try to rebuild after such a severe drought (assuming it ends in March 2023), Mr Quilty said.

This would see peak global meat prices in 2027.

“This rise in US pricing will soften the Australian livestock price falls and enhance the price rises for Australian sheep and cattle during that five-year period,” he said.

“The question remains on the capacity of beef and sheep processing plants in Australia over the next five years and the tight labour problem. Will this see too much processing capacity in cattle and not enough in sheep on the Eastern Seaboard? Time will tell, but I can’t help thinking that dual species operators will have a comparative advantage with flexible labour.”

He predicted that the restocker will re-emerge with a vengeance in 2026 and 2027 after an anticipated subdued 2023 to 2025 period.

“The restocker will have fewer cattle and more grass, and human nature will see them be equally aggressive in 2026 and 2027 as they have been in the last two years. The role of the lotfeeder will also remain critical once again in this period, as the market looks to add value to fewer animals.”

“I will be watching each August closely on the release of this ABS data on land use and the potential ongoing changes that may occur. These changes are likely to be long-term and structural – meaning that the availability of land for grazing is getting tighter, which will limit the growth of Australia’s sheep flock and cattle herds in years to come,” Mr Quilty said.

The outlook over the long term was for stronger livestock prices and increasing land values.

“It’s often the way when resources become limited and demand remains strong,” he said.

HAVE YOUR SAY