PRICES for imported lean grinding beef have spiked sharply in the US over the past fortnight, as record high meat-block formulation prices cause some panic among US grinders and other end-users.

Short-bought buyers finally decided to come into the market in order to cover needs last week, analysts reported.

“They’re finding that offerings from Australia remain limited, even as export data from Australia points to a surge in overall beef shipments to the US, particularly shipments of lean grinding beef,” Steiner Consulting reported in its weekly US imported beef report.

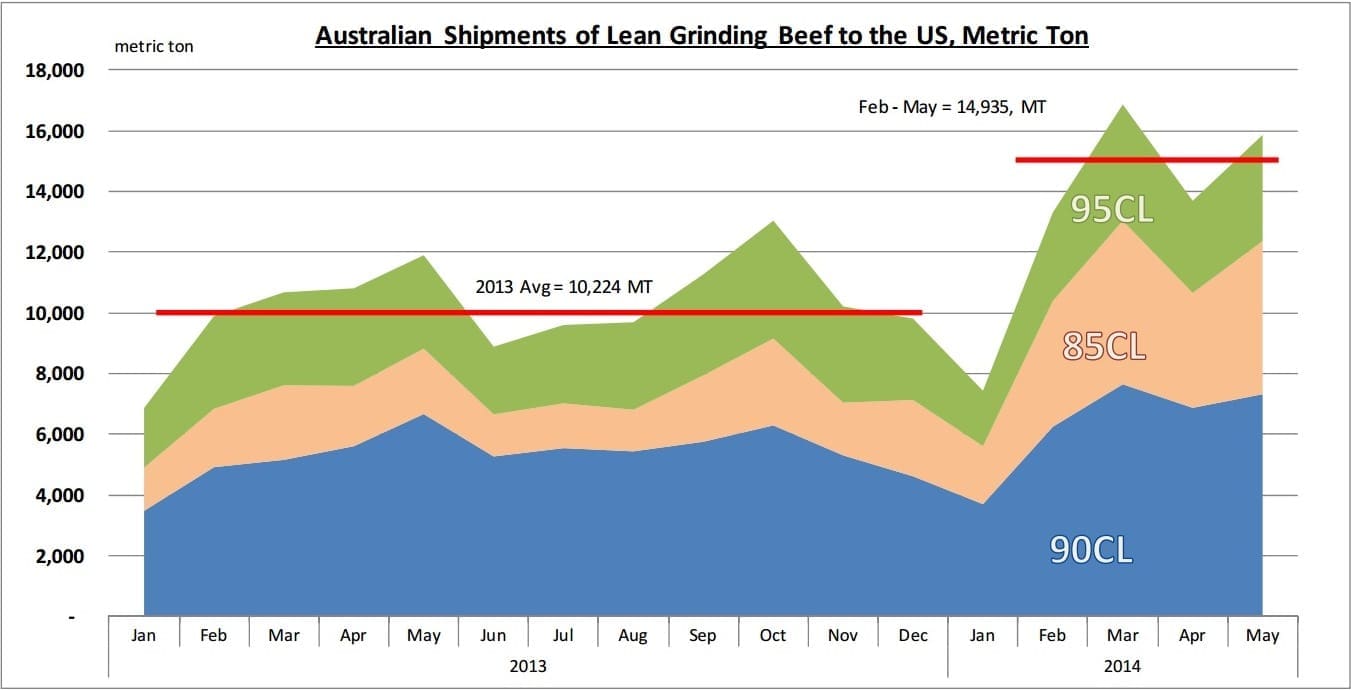

Australian export data shows that shipments of lean grinding beef to the US (85, 90 and 95CL product) reached 15,867 tonnes in May, 33 percent higher than a year ago.

Indeed, during the February to May period this year, Australian monthly shipments of lean grinding beef to the US have averaged almost 15,000t. That compares to a monthly average of around 10,000t in 2013.

“This implies that for each month, there is an additional 260 truckloads of imported lean grinding beef in the US,” Steiner’s report said.

This additional volume has caused imported product to trade at a significant discount to US domestic product. The discount in some cases has been as large as US40c/lb (88c/kg), the largest discount of the past 20 years or so, Steiner reported.

In the last two weeks however, prices for imported lean grinding beef in the US have surged by as much as US12c/lb. A number of factors have contributed to the ‘suddenly impossible to buy’ market for imported beef:

- Some US end-users are short-bought and this has caused something of a covering rally.

- US domestic grinding beef prices have moved counter-seasonally higher in June. There is a tendency for US lean beef prices to drift lower after Memorial Day holiday, and some end-users were hoping to grab product at lower prices. That did not happen, and users are now scrambling to find product

- There appears to have been some delays in deliveries, meaning traders/suppliers are looking for available product to deliver to regular customers

- The implied 76CL meat block cost (the blend of US fatty trim and imported lean trim, required to deliver the ideal beef patty) is currently up 27pc compared to a year ago. So far, fast food operators have struggled to manage costs and there are concerns that there will be little relief in terms of prices and supplies until late in the fall. This has likely made for more aggressive bids.

- New Zealand supplies are expected to decline sharply in late June and July. While slaughter last week in NZ was a little over 60,000 head and 15pc higher than a year ago, numbers are likely to be cut in half in the next four to five weeks, as the season draws to a close.

- Some US market participants are pointing out that the dearth of offerings from Australia may represent an effort to try to keep the market up, knowing that NZ supplies will be seasonally lower in July, while other supplies (Uruguay, Mexico, Central America) remain limited and are bringing less volume than last year. While this may be the case with individual packers, the export data from Australia tells a different story. Australian shipments to the US in June again look like surpassing 30,000t and grinding beef will likely make up about be about 25,000t of that. Total monthly exports by June 20 had already reached 24,000t. Rather than holding back, it appears, that a larger portion of the imported business is by-passing the imported beef trade and delivered directly from Australian suppliers to US end-users.

Click on images below for a larger view

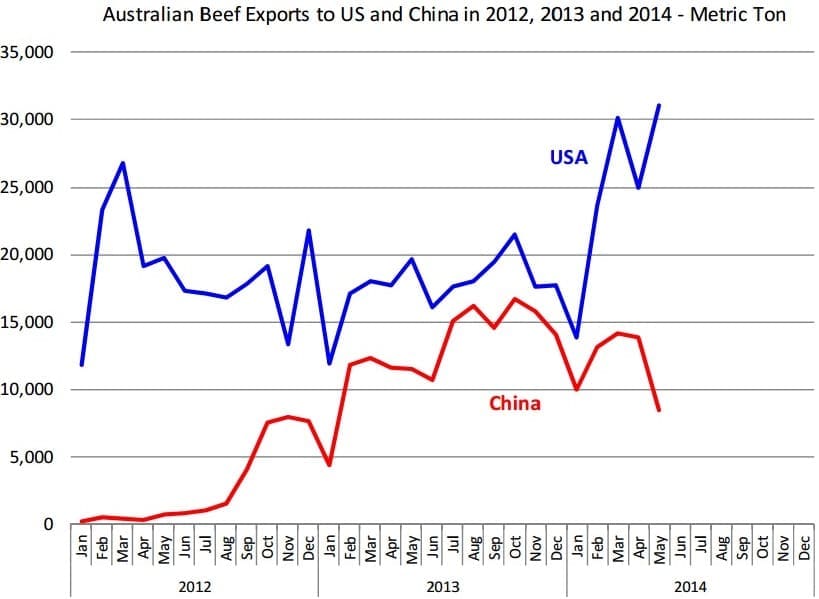

High prices in the US certainly have encouraged more Australian beef to come to the US. The chart here shows the surge in beef shipments to the US while exports to China have slumped. The May decline in exports to China was due to new measures taken by China with regard to HGPs. It remains to be seen how Australian beef exports to China proceed in the coming months. The big wild-card in Australian exports remains weather. Drought conditions have forced producers to send more cattle to market and at this point it is a guessing game as to what moisture conditions will look like in Australia’s late winter and early spring.

“The bottom line is that imported beef availability in the US is limited, even as Australia ships significantly more product than it did a year ago,” Steiner’s weekly report for MLA said.

“Much of product coming in is already spoken-for, and short-bought users are having to increase their bids in an effort to secure product,” the report said. “High domestic prices remain supportive and ongoing short cow slaughter levels all but assure record high cow meat prices in the US this summer.”

HAVE YOUR SAY