GLOBAL negativity and offshore events led to limited wool forward market bids last week.

GLOBAL negativity and offshore events led to limited wool forward market bids last week.

Predictably, the spot market was unable to withstand the global negativity and remains at the mercy of off shore events.

This spilt over into the forward markets with the limited bids getting hit as the market failed to find a level.

Volatility is running at historically high levels. The challenge for the forward market and for all participants from grower to processor will be trying to find fair value levels to mitigate and spread some of the risk. Just where this level will be found is difficult to predict.

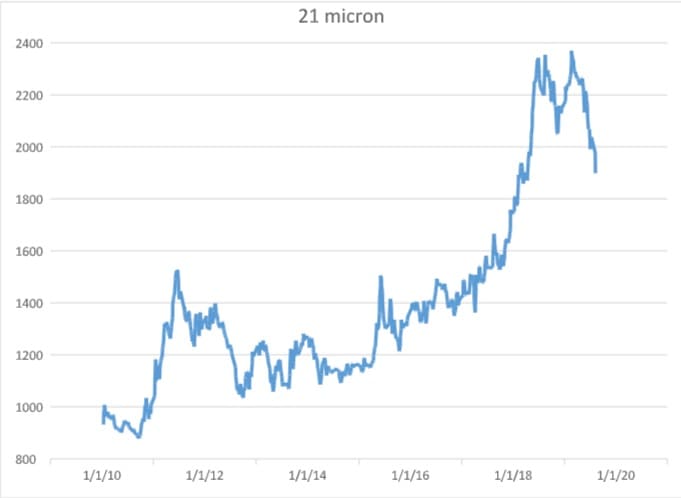

As mentioned in our season closing technical analysis, where looking at various retracement levels as the market had broken its long-term uptrend. On the key microns (19 and 21) the first retracement to 2180 cents and 2080 cents had been breached.

This week’s market fall has taken out the second support level of 2010 cents for 19 microns. The 21 micron index currently sits right on support at 1900 cents. The next technical level is 1735 cents for 19 micron and 1620 cents for 21.0 micron.

This technical analysis needs to be weighed against the current supply situation and the factors influencing demand. Drought-induced tight supply will not improve in the short to medium and likely to be in the order of another 5 to 10 percent year-on-year. Recent disease and subsequent financing issues out of South Africa will tightened short term supply further.

Our real concern when evaluating price risk at this point is the assessment of demand. Current trade tensions, political instability and lack of confidence right through to the consumer is affecting all commodity markets.

The key now is to develop a risk strategy and be prepared for the volatility that is likely to occur over the season. Demand will ebb and flow, but supply will remain tight. This should present opportunities for growers to cover forward.

Next week’s levels will rely on the off shore reaction to this week’s decline. At present there are no forward bids. Prices have fallen to 18-month lows, but processors are quick to cite that they are still above the 80th percentile for the last decade.

We expect tentative bidding to come in around 100 cents under cash, but to be sensitive to further movement. The main Merino indices lost 70-140 cents this last week. The market unfortunately will be at the mercy of outside influences again. Let’s hope for more sensible rhetoric and a calming of trade tensions.

Trade summary

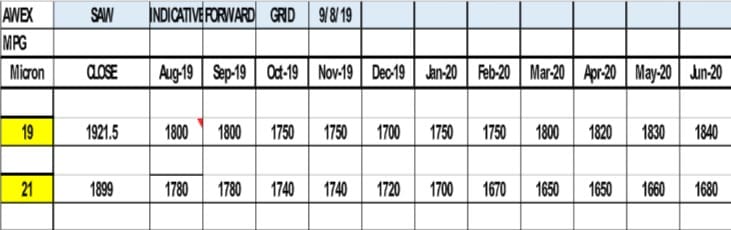

19 micron August 1920 cents 2 tonnes

October 1865/1920 cents 10 tonnes

21 micron September 1850 cents 10 tonnes

October 1865/1930 cents 15 tonnes

Total 37 tonnes

HAVE YOUR SAY