Southern Aurora Markets partner Mike Avery.

FORWARD wool market trading extended into next year in another week dominated by global sentiment and rhetoric.

Most soft commodities had positive price movements off the back of US Federal Reserve comments on a steadying trend in interest rates.

A weaker USD pushing cotton prices along with continued optimism of an easing of the COVID restrictions in the dominant manufacturing and consumer market of China.

That optimism has not been reflected at wool auctions with the market giving up the gains of last week and a little more to boot. The run into the recess is likely to be a balancing act with the normal positive tone that accompanies the path to Christmas facing increasing short-term headwinds.

The weak USD will tend to hamper those processors looking to commit to their New Year buying program. Lack of clarity around domestic restrictions in China is still in the front of mind of many.

On the forward market front, it was pleasing to see activity out into the Spring and Summer of 2023.

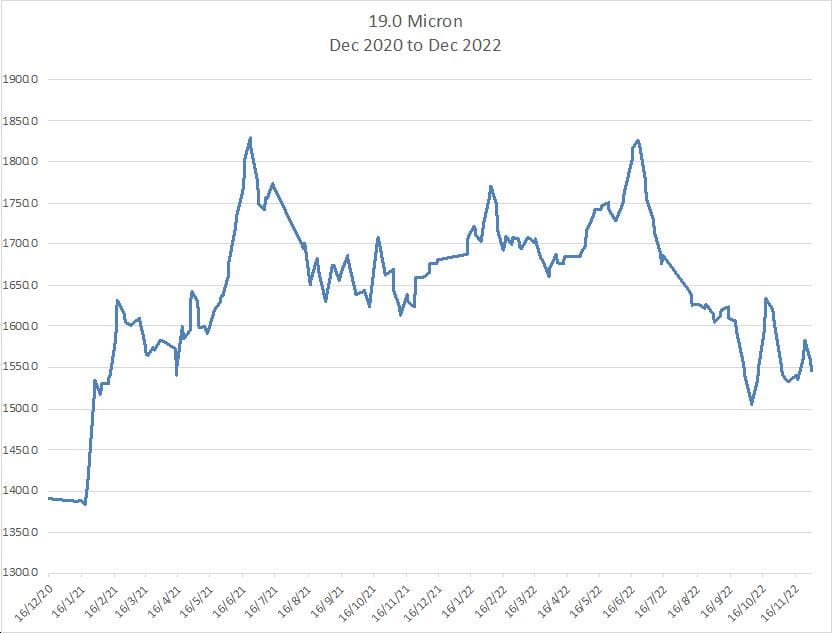

September through to December traded at 1550 cents for 19 micron (current spot 1545 cents). Just as important is the bidding for the whole of 2024 (January to December) is based at that same level. The above tracks the 19 micron prices for the last two years. Whilst the trend is definitely negative, and the current headwinds could see a temporary break below the most recent support level (1500 cents) the forward market is indicating a stabilisation around that level.

Current bidding for December and indications for early in the New Year has exporters and processors looking for a further pull back of 2 to 3 percent before we see a base form. On the main traded microns that is around 1500-1510 cents for 19 micron and 1250-1260 cents for 21 micron.

Trades this week

December 2022 19.5 micron 1435 cents 5 tonnes

September 2023 19 micron 1550 cents 10 tonnes

October 2023 19 micron 1550 cents 10 tonnes

November 2023 19 micron 1550 cents 10 tonnes

December 2023 19 micron 1550 cents 10 tonnes

Total 45 tonnes

HAVE YOUR SAY