Southern Aurora Markets partner Mike Avery.

A WEEK is a long time in all markets these days, and consistent falls plague almost all agricultural commodities.

A strong Australian dollar had supported the wool market after the Easter recess, providing a flat to premium curve on the forward market and confidence that we were moving through the strong supply period unscathed.

However, the hard-earned gains of the previous five auction sessions were given back this week.

Demand remains steady at best and the market remains vulnerable to outside influences. These came thick and fast, with concerns over USA finances and poor Chinese trade figures headlining the general negative tone of global reports.

The forward markets pre-empted the softer auction market, with sellers taking out the best bids available prior to the opening Tuesday.

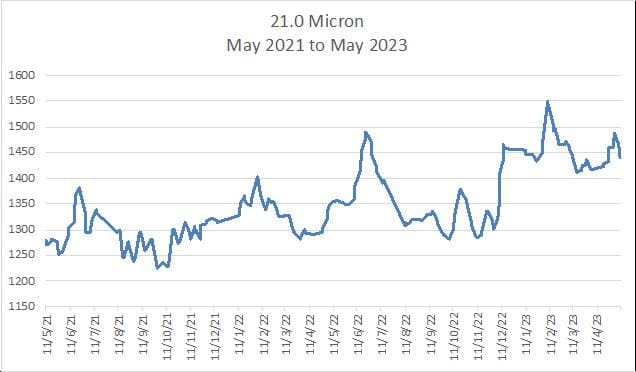

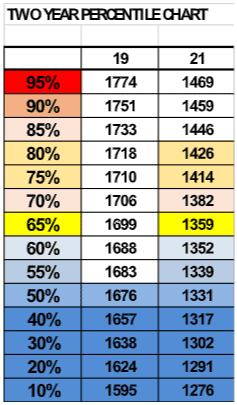

The majority of trades centred around the strong bidding on the 19 micron contract. Twenty tonnes were executed at 1660 cents (47 cents over the close of 1613 cents) in December and the first quarter of 2024. Bidding for the remainder of 2024 and the first half of 2025 is still at a 1 percent premium to cash at 1630 cents, reflecting the weakness in the spot market.

Generally, sellers remain resilient with passed in rates at auction high and forward levels not discounted.

It is difficult to see the situation changing, with close to 50,000 bales on offer next week. Exporters continue to struggle under the financing pressure of extended cycle times (purchase to payment) with dumps and packers continually stretched. Front months are now bid around 30 cents under cash and offered flat to cash. Spring growers are looking to hedge flat to cash but exporters and processors are unable to match and are yet to show their hand to any degree.

Currency movements will only mask the general trend which looks to continue in a negative direction.

The wool market will remain at the whim of macro-economic and political sentiment which continues ebb and flow. Reducing risk and providing margin certainty seems to be on the agenda, but buyers and sellers are finding it difficult to ascertain fair value.

This week’s trades

May 19.5 micron 1560 cents 2.5 tonnes

Dec 19 micron 1660 cents 5 tonnes

January 2024 19 micron 1660 cents 5 tonnes

February 2024 19 micron 1660 cents 5 tonnes

March 2024 19 micron 1660 cents 5 tonnes

Total 22.5 tonnes

A strong Australian dollar had supported the wool market after the Easter recess, providing a flat to premium curve on the forward market and confidence that we were moving through the strong supply period unscathed.

However, the hard-earned gains of the previous five auction sessions were give back this week.

Demand remains steady at best and the market remains vulnerable to outside influences. These came thick and fast, with concerns over USA finances and poor Chinese trade figures headlining the general negative tone of global reports.

The forward markets pre-empted the softer auction market, with sellers taking out the best bids available prior to the opening Tuesday.

The majority of trades centred around the strong bidding on the 19 micron contract. Twenty tonnes were executed at 1660 cents (47 cents over the close of 1613 cents) in December and the first quarter of 2024. Bidding for the remainder of 2024 and the first half of 2025 is still at a 1 percent premium to cash at 1630 cents, reflecting the weakness in the spot market.

Generally, sellers remain resilient with passed in rates at auction high and forward levels not discounted.

It is difficult to see the situation changing, with close to 50,000 bales on offer next week. Exporters continue to struggle under the financing pressure of extended cycle times (purchase to payment) with dumps and packers continually stretched. Front months are now bid around 30 cents under cash and offered flat to cash. Spring growers are looking to hedge flat to cash but exporters and processors are unable to match and are yet to show their hand to any degree.

Currency movements will only mask the general trend which looks to continue in a negative direction.

The wool market will remain at the whim of macro-economic and political sentiment which continues ebb and flow. Reducing risk and providing margin certainty seems to be on the agenda, but buyers and sellers are finding it difficult to ascertain fair value.

This week’s trades

May 19.5 micron 1560 cents 2.5 tonnes

Dec 19 micron 1660 cents 5 tonnes

January 2024 19 micron 1660 cents 5 tonnes

February 2024 19 micron 1660 cents 5 tonnes

March 2024 19 micron 1660 cents 5 tonnes

Total 22.5 tonnes

Source – Southern Aurora Markets.

HAVE YOUR SAY