Old fashioned business sense – As a seller or a buyer why didn’t you sign a contract ? Too busy, they are old fashioned, agent didn’t have one, don’t understand them? ‘I confirmed it on my mobile phone with a phone call’ etc etc. Ever tried buying a car or land without a contract?

The recent reset of prices shows the importance of signing a contract. Each load of livestock is worth between $120,000 and $200,000 yet we seem to think a “nod and a wink” will hold up when the market corrects up or down by $1 a kilo liveweight. Rainbows and unicorns don’t help anyone in this circumstance.

Do yourself a favour; whether you are an agent, farmer, processor or lotfeeder, get contracts signed and remove the heart ache of “I didn’t think the market would move that much.” And remember – no signature, physical or electronic, no contract when you try to enforce it.

Around the traps

Phil Kelly and Matt Keely from Colliers in Queensland dropped me a note on a recent tour through the Darling downs, Central Highlands and Maranoa.

“Looks like many will be eating Christmas ham on the header.

“Summer crops are starting to move and there seems to be a significant amount of new country being planted,” he said.

“Not a lot of stock observed from the road until into the highlands.”

I also caught up with my old work mate Robbie Neale, Gorst Rural at Lake Bolac in Victoria’s Western Districts for a client breakfast with 70 attending. It was a great morning talking about the benefits of converting pasture growth to weight gain aligned to a target market. Conditions were very wet, but all are positive and thinking about producing more off the same number of acres.

I checked my thoughts with Andrew Hosken from Hosken Stock and Land, Agency and consultancy at Tamworth who has always provided me with a great balanced view.

Current market dynamics

- Extended high prices from Australia supplying meat both nationally and internationally – “at various times the dearest in the world”.

- Present feedlot exits are amongst the dearest ever seen. Go back 150-200 days ago when entry level feeders may have gone in at up to $6-7/kg LW. Feedlots are bleeding!

- A better season has led to higher carcass weights— more meat to move. A wet season saw most stock perform slowly through winter & spring. How many of those trading stock are still in the system?

US market drivers

- Continues to have dry conditions and high turn off into feedlots

- The follow-on increased weights in kills of high-quality product (from more days on feed).

- When their feedlots further empty there will be less availability of replacement stock.

Leading to medium term drop off in their production & increased opportunity for us.

Looking forward – Do not panic. Our fundamentals remain strong.

- Make sure you have lifetime traceability – within breeding operations as well as trading stock.

- Register for the many grass-specific programs across a number of processors.

- Monitor opportunities and consider different trades.

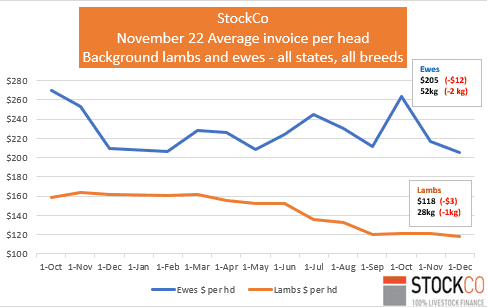

Sheep and lamb

The recent reset on price will allow us all to go into the new year with a positive margin opportunity on trading. At current store prices, there is still a margin even if selling lambs at $6.50$7/kg cwt. Mutton in the low $4/kg is a no-brainer. After the long weekend in January the southern pastures weight gain fades quickly and grain feeders start to reload for the Winter.

There is lots of heavy mutton at present that I see as an opportunity. It takes the same amount of feed to keep them fat as it does to keep them skinny. Buy some Merinos, shear five kilograms of wool and take the heavy mutton price in winter.

Lamb shearing is still an issue in many areas and the difference in store prices between woolly and shorn is significant. I am still very confident on the opportunities to trade lambs at current values for supply into next year. I see two distinct models appearing:

- Buying lambs with weight and improve on grass / bean stubble to sell into a short term trade/heavy order.

- Buy lighter lambs – dollar value makes these very attractive. Then sell into the store market at 40-45 kg. Don’t try to fatten them. Take the margin and move on.

Saleyards versus over the hooks

I tend to skip through survey presentations, but the recent Sheep Central article about the Sheep Producer Intentions Survey left me thinking maybe I have been watching the wrong game. I am not going to jump into a full analysis, but I do want to raise several points. It seems this high-level survey has missed some key observation headings.

Last year’s leviable transactions provide a great base line, but I cannot find them anywhere as a reference. We then move onto missing segregation of prime stock and store stock with a mixed understanding of what is meant by hook, private sale, auction when talking about sale yards. Without doing this, the direct to slaughter (hooks) sale numbers become diluted. The assumptions about saleyard numbers also missed some key driver understanding and, in my belief, paint an incorrect state of play.

- This year the season has produced significantly more store lambs targeted through saleyards, private sale and AuctionsPlus.

- Also there have been no light lamb airfreight orders operating.

- These lambs therefore increase the number of lamb transactions as they become two and sometimes three sales of the same lamb before processing.

- Over the past 15 years a significant trend has appeared with finished lambs being sold over hooks through a forward contract.

- Saleyards are an excellent price discovery tool in times of short supply, but currently are a necessary evil to move lambs on a falling market that must be sold because of feed, harvest, fly worries etc etc and limited slaughter space.

- This year the season and condensed supply has push lambs to saleyards because of limited kill space through capacity and a need to sell. In turn processors have moved contracted lambs back to capitalise on the lower saleyard pricing – Catch 22.

- Producers have feed with lambs that have not done during wet weather, so we all held on.

- It is highly unlikely we will see this repeat next year under a normal season as we should revert to a progressive selling pattern that moves from (Southern Australia) north to south spreading out the numbers.

- This benefits producer and processors with a pricing and supply continuity – manageable supply flow

- The impact of the Foot and Mouth Disease scare in July has been significantly understated regarding the abnormal sell off of unfinished lambs and the associated fall in price that we did not recover from.

- Why wouldn’t the stock agents and processors have been surveyed on what their sale break downs are, which would provide fact-based detail?

As I have said in the past it is very easy for information that is collated for the right reasons to paint the wrong picture – especially when being read by policy makers that may not understand the industry. Just because it exists does not mean it is right.

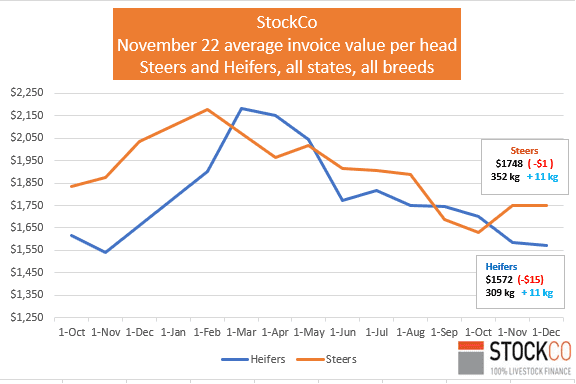

Cattle

The feedlot price reset has arrived with numbers held back by rain arriving in force. Many lots are on no quote and becoming extremely selective on quality. Cows have eased by a full dollar and will probably soften more as numbers appear pre the southern weaner sales.

Those trying to off load mixed runs of crossy cows PTIC of CAF into the store scene are starting to struggle as the price slips. Quality straight runs are still in demand especially with calf at foot.

First of the weaner sales – Spence Dix and Co’s Jonathon Spence, Keith said buying support for the recent Moville/Amherst weaner sale was still strong with the south-east South Australia, Gippsland, Mildura, Jamestown and feedlot support from TFI and JBS. Heifer support came from central NSW. Prices were $180/$200 per head softer than a month prior. However, the Johnson families weaning protocols of 7-8 weeks off mum paid dividends with buyer confidence knowing the calves would not lose weight once home. Best heavy feeder steers made to $5.80 with most prices ranging from $5.50 to $6 for the lighter end.

Miller, Whan and John director Andrew Whan at Mt Gambier (and RMA president) attended last week’s Naracoorte weaner sale. The yarding presented steers and heifers with a notable premium for EU cattle. Two orders operated out of NSW with local and Victorian buyers bidding at reduced rates in line with the last two weeks’ reports. Auctioneers had to work hard and those that had orders in place to cover their yarding were rewarded. The top of the heavy weaners weighed 370 kg and ranged from $5.20-$5.40 with the mid-range 300kg plus $5.20-$5.50. Under 280kg achieved $5.70-$6. Heifers sold at rates equivalent to steers with well-bred Angus sought after as future breeders. Andrew also flagged the Mt Gambier Angus weaner sale on this Friday the 9th with 3800 across all agents being offered at the Glenburnie yards.

Naracoorte PPHS agent Ashley Braun let me know PPHS will present its 1st annual sale comprising of 2800 steers and 800 heifer weaners this Thursday the 8th. With the growth of the Naracoorte numbers over time this stand-alone sale allows all calves over the two weeks to be presented in the best way for breeders.

Weaner sales – Don’t run away from buying, but reset your pricing expectations for this year’s sales in advance. It looks as though we will be closer to the 2020/21 pricing than what we saw this year. Weaning will pay dividends; however, mixed colour runs might see a discount if not presented correctly in the yards or on AuctionsPlus.

- Watch the first VIC weaner sale of the season live via our Facebook page on Wednesday morning: Murray Arnel will be covering the first of the new season weaner sales at Euroa for Beef Central THIS morning and will be livestreaming the sale via the Beef Central Facebook page from 10am – click on our page (link here) to follow the sale live with Murray

Strategic thinking and analysis

Often we see things happen that appear to have landed on us out of nowhere because we are focused on our day to day tasks, jobs or operations. It is rare we take time to think about our business strategy and rarely about industry level strategies – exporters, processors, feedlots, banks, government etc. I am not suggesting you try to change a particular company’s strategic direction but if you think about why they need to do something often it provides you with an answer to what your operation should be mindful of. We love to call it “luck” in Australia when someone reads the market well instead of recognising it as a well executed business plan.

If you look at interruption to our trade in recent times we have been given several good indicators of what might be over the horizon. One being the recent FMD scare showing us how fast the market can fall on the back of additional numbers hitting the scene. Cattle recovered for a period with the continued wet however lamb and mutton pricing continued to struggle under the numbers back log.

Another example is the impact of a trading partner “pulling up” on buying meat – look at the goat prices as an example.

It is highly unlikely that a trading partner woke up and said “lets crack Australia off today.” Often this one action is part of a significant strategic placement piece or logistical blockage that encompasses a much wider scope than we are aware of. I did note in the early days that the progressive closing of our export commodities to one country was in alphabetical order.

The livestock supply chain is no different – larger companies have boards that determine the strategy and direction for an extended period and the ground troops deliver the operational outcomes. All of the well run family farming operations I know have adopted this structure. Allowing the overarching strategy to be put in place well in advance.

Accountability to deliver becomes the main driver under this structure – Where is our business heading, what does it look like, what is required, what did you do and what was the outcome. If you think adopting this model for your enterprise works look for a set of “outside eyes” for your board that will ask the hard questions, employ subject matter experts when you need to verify your thoughts – and plan to succeed.

Supply, demand, logistics, high input costs and price resistance have now merged to deliver a market correction on lambs, cattle and sheep that without the continued rain would have happened in March and September. We are now observing livestock being held because the price is not palatable compared to 2 months ago yet in 2019 / 20 it was acceptable and you would have happily sold. If you are leaving your stock in the paddock because you are going to ride out the price with your excess feed make sure you have 4 – 6 months in front of you.

Instead of holding your stock consider selling your own home bred and buy in a trade at less value that provides you with a weight gain and margin window.

Opportunities

- Sell your own and use your feed to create a trade

- Monitor opportunities and consider different trade types.

- Do the numbers on putting more weight on if the price continues to ease – is it worth the extra risk

- Don’t be scared to buy light lambs to improve and sell as heavier stores in 2023

- Start thinking about supplying into the Southern winter short supply period – only 6 months away.

- Buy heavy mutton to re-sell after easter

- Keep drafting your dry cows off before the weaner sale run of cows appear

- You can’t change the price, but you can reset and think about the opportunity

- Let’s put a line through 2022, enjoy Christmas, stay positive and look forward to a new year

- New Agency training group 20th February start at Wodonga

That was a really good update Chris

Thank you