Simon Quilty

Global currencies and stock markets have weakened over the past two days as financial markets have deep concerns about the ramifications of the latest stage in the US China trade war. “So far Australia has been a beneficiary of this new chapter in the war, but if we are not careful this could be short-lived,” independent meat and livestock market analyst Simon Quilty warns in this report …

THE global trade war between China and the US in the last few days has taken on a new twist that has seen China devalue its currency against the US in retaliation to the 10pc of additional tariffs the US has placed on $300 billion worth of Chinese imports to be introduced from September 1.

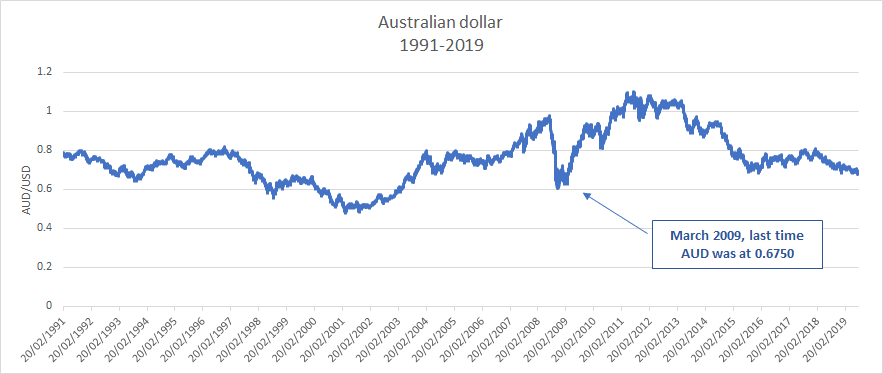

Global currencies and stock markets have weakened over the past two days as financial markets have deep concerns about the ramifications of this next stage, with the A$ yesterday at US67.5c – falling 4pc in the last two weeks from US70.3c.

So far Australia has been a beneficiary of this new chapter in the trade war, but if we are not careful this could be short-lived. Investment bank Cowen Inc analyst Chris Krueger on Monday said the US Fed is likely to cut interest rates in September, which he stated was to “offset the drag caused by this escalation in the trade war.” But to me, it is really about cheapening the US$ and it is for this reason that I believe the Reserve Bank of Australia has been lowering interest rates in an attempt to pre-empt what we are seeing this week.

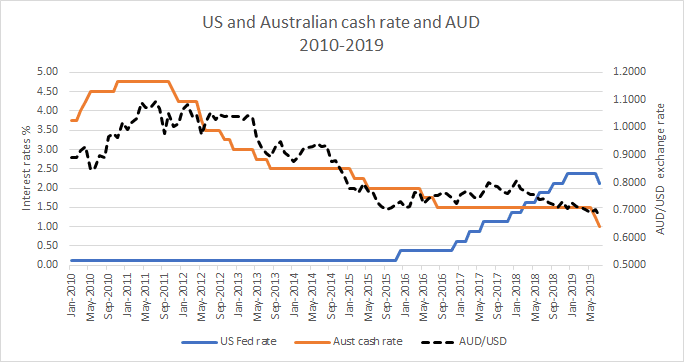

Yesterday, the Reserve Bank decided to take a pause and not lower interest rates – for good reason. The problem is that Australia’s official cash rate is at 1pc and that the US Fed rate is at 2.25pc, and therefore Australia has little room to move if the US lowers interest rates further.

It will eventually see the A$ move higher if we cannot keep pace on interest rates. Welcome to a currency trade war that Australia will be caught up in, but can do little to prevent or stop.

The ramifications on Australia’s meat and livestock industries is enormous, with currency movements, the lower we go in terms of currency the higher becomes the domestic value of our product.

I estimate a 100 point movement (i.e. our currency moving from US68c to US67c) in the A$ would see slaughter cattle (cows in particular) liveweight prices go up by 12c/kg carcase weight, or 6c/kg liveweight – in a ‘perfect world’. Sheepmeat would be similar, I suspect.

Our beef supply competitors’ currency movements are of equal importance. If they should weaken more than Australia against the US$, then we are at a disadvantage. Equally, should they go higher, then we have a comparative advantage. As an example, Argentina’s currency has fallen 55pc since the global trade war began.

The impact of key beef market buyers’ currencies is also important, as their buying power goes up and down depending on the value of their own currency. This is particularly important for our export markets including Japan, China, US and Korea.

Japan and the US currencies are relatively firm compared to Australia, which is good for Australian beef exports, given that we dominate both these countries as beef suppliers and our major competitor is the US, which has a much higher currency.

South American countries’ currencies have devalued anywhere from 17-55pc since the trade war began last year, and as a result have a significant advantage over Australian beef exports in China.

Our greatest concern is that the US looks to lower interest rates as a means of devaluing the US$, and results in US interest rates below Australia’s interest rates. This would see the A$ rise dramatically, and could see our currency close to parity – similar to the 2011-2013 period which saw the A$ average US103c.

If the A$ was to go to parity, this could remove close to 30pc off livestock prices in Australia, should all other variables remain constant.

President Trump and many of his Republican allies have had real concerns on currency manipulation for many years, and have started to try to embed into free trade agreements clauses which prevent manipulations occurring. So far most countries have refused to accept these clauses.

Impact on Australia’s meat and livestock sector

As stated earlier, the ramifications on Australia’s meat and livestock is enormous, as the lower we go in terms of currency value the higher the domestic value is of our meat and livestock.

There are always many variables impacting cattle prices based on weather, local demand and other markets needs, and customers’ respective currencies, but if all variables were held constant then 12 c/kg on carcase weight is the likely livestock upward movements and therefore a 300-point fall in the A$ in the last two weeks should (all other variables aside) see prices improve by 36c/kg CW, or 18 c/kg LW. In reality, the world is far from ‘perfect’, however, and other influences are still reflected in cattle price.

Relationship between cattle supply and currency benefit

What is also important to note is the tighter the cattle supply, the more likely it is that the full benefit of a fall in currency will be passed back to producers. If cattle are in over-supply and therefore meat is in over-supply, then the benefits are often shared between importers, processors and traders. As a rule of thumb, the more plentiful cattle/meat supply is, the more these currency benefits are passed forward to the buyer and conversely, the tighter the supply the more benefits passed back to the producer.

Impact on our competitors of the currency war

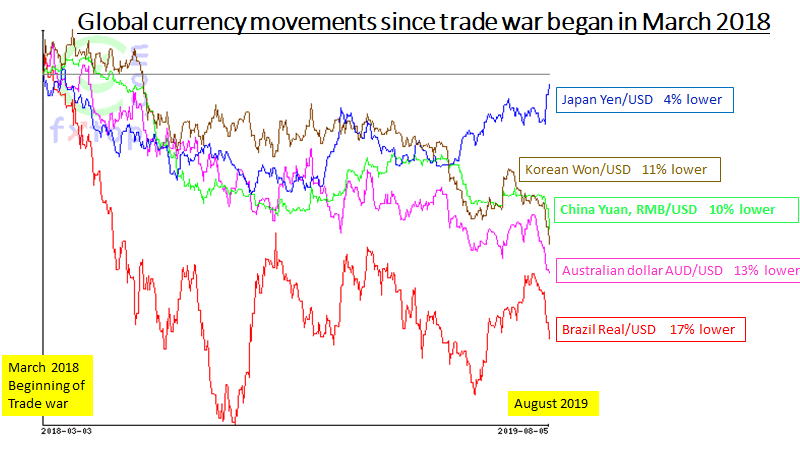

The impact on our export competitors’ currencies has been varied since the trade war began in March 2018, when President Trump introduced a 25pc duty on steel tariffs.

Key points to note:

- Argentina’s currency has more than halved in value since March 2018. Much of this is related to domestic problems with high inflation rates and a recession and has seen close to 75pc of all Argentina’s beef exports go to China.

- Brazil’s currency has fallen almost 18pc since March 2018, compared with Australia’s 13pc, which has seen Brazil market share in China remain at 19pc – almost identical to Australia’s and Argentina’s.

- Canada, New Zealand and India have all had currency devaluations but not as large as Australia’s, which has ensured Australia maintains a competitive edge over these rivals.

Australian meat export competitors currency change

Last 6 months currency movement

Currency movement since trade war began March 2018

Impact on our key beef markets

The impact of falling currencies is just as important in the markets we sell to, and these recent currency movements have seen in some instances Australia achieving some gains and in others markets some setbacks.

Points to note:

The US is our largest competitor in both Japan and Korea, and since March 2018, the Japanese Yen is 4pc lower and the Korean Won 11pc lower, and with an A$ at 13pc lower, we are significantly cheaper and more competitive into both these markets compared to the US.

Unfortunately Australia’s role in these markets has been challenged, as consumers in both countries have shown a genuine preference for US beef which has seen higher US prices make up for this lost ground.

The other key market is China, with the yuan having fallen 10pc since March 2018 and with South American supply countries dominating the China import beef market and their respective currencies falling 17-55pc in value. It is hard to claw back the current 60pc beef import market share they enjoy – Australia’s market share of China’s beef imports currently sits close to 20pc, and should South America’s currencies fall further and/or Australia supply tightens, it will be hard to maintain this share.

Where is this trade war likely to go?

The real concern is if the US tries to devalue its own currency in an attempt to counter-punch China to make US exports more competitive, imports less attractive, protect US jobs and stimulate the US economy through cheaper and more competitive exports – thereby ‘making America great again’.

The most common form of devaluation is through quantitative easing, which we witnessed during the post 2008 financial crisis period. This saw the A$ during the 2011-2013 period go to parity or higher, and made Australian exports very uncompetitive globally.

Should the US try a similar strategy again, it would seem likely that China would peg the yuan to the US$ and therefore move in tandem, giving no competitive benefit to the US over China. Instead what would likely happen is that the A$ and all other commodity related currencies would move higher as the two currency heavyweights – US and China – go toe-to-toe. Australia could become a casualty of this currency war.

As stated earlier, the problem is that Australia’s official cash rate is at 1pc, while the US Fed rate is 2.25pc, and therefore Australia has little room to move if the US keeps lowering interest rates further. It will eventually see the A$ move higher if we cannot keep pace on interest rates.

We saw this after the global financial crisis where the US government lowered interest rates to almost zero, which in turn saw the A$ trade above parity for almost three years. Let’s hope we don’t return to parity again, but for the same reasons that a 100-point A$ fall might see a 6c/kg rise in livestock prices, the reverse can easily happen where by a return to parity for the A$ could see close to 30pc wiped from livestock values in Australia.

Currencies have been a bugbear of President Trump for a long time

President Trump and many of his Republicans colleagues have had a ‘bugbear’ on China’s manipulation of currencies for many years, and this week the US Treasury came out and stated that China was a ‘currency manipulator’. Secretary Mnuchin announced that he would engage the International Monetary Fund to eliminate the unfair competitive advantage created by China’s latest actions.

The US Treasury went on to say that the purpose of China’s devaluation was to gain an unfair advantage in international trade. On Monday the yuan fell to 7 against the US$ for the first time since 2008.

The talk of currencies has been at the forefront of the Trump Administration, which under almost all recently-negotiated free trade agreements has asked for a currency clause. This was the case recently in negotiations with Japan, China, Canada and Mexico, whereby US negotiators asked for a currency clause to attempt to prevent competitive devaluations from occurring. Japan strongly opposed this clause, believing that it would tie the Bank of Japan’s hands and claiming that currency moves and export volumes don’t correlate.

In recent times the US Department of Commerce has been looking to go a step further, and place tariffs on all trading partners that devalue their currency, treating such practices as subsidies. This week’s reaction by the US is testimony to this.

Conclusion

In the long-term, I don’t think there are any winners in a currency war – only losers as trade flows become distorted and smaller countries like Australia get caught up in the crossfire of this trade war.

I have no doubt that recent decisions by the Reserve Bank of Australia to lower Australia’s interest rates have been strongly influenced by the concerns of a currency trade war. Yesterday’s decision to not lower the official cash rate, I believe, is to ensure that Australia does not fire ‘all our interest rate bullets’ too early. Being only at 1pc, we do not have much room to move.

The underlying concern is if US interest rates go below Australia’s, which will inevitably see the A$ move higher, and possibly towards parity. Yet, as stated, China can easily counter this by simply pegging itself to the US$. In the meantime global growth is likely to suffer and the possibility of a global recession starts to become a reality.

Nice analysis Mr Quilty. As you say, it seems obvious China would peg their currency to the US dollar in a race to the bottom, so what other options do the US have? Cheers