The official commodities forecaster said the predicted fall reflects lower prices across most livestock and livestock product categories more than offsetting higher levels of production.

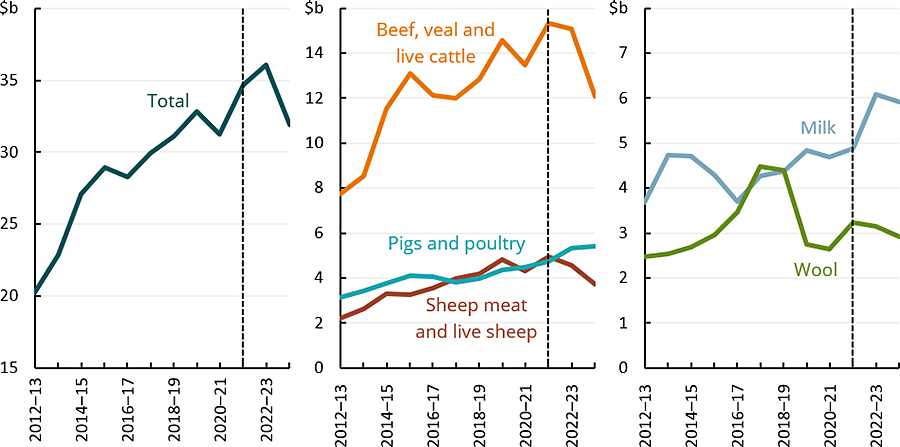

The forecast fall in the gross value of production is driven by beef, veal and live cattle (down 20pc to $12.1 billion) as well as sheep meat and live sheep (down 19pc to $3.7 billion). Lower production values are also forecast for milk (down 3pc to $5.9 billion) and wool (down 7pc to $2.9 billion). However, the production value of pork and poultry meat is expected to rise (up 1pc to $5.4 billion).

The forecast value of livestock and livestock product production in 2023–24 is $2.1 billion lower than in the September Agricultural Commodities Report. A downwards adjustment to average saleyard prices for livestock – reflecting recent price data – has more than offset a small upwards revision in production.

Figure 1.1 Annual value of livestock production and livestock products

Source: ABARES; ABS

The value of livestock and livestock product exports is forecast to fall to $27.7 billion in 2023–24, down by 1% from $27.8 billion in 2022–23 (Figure 1.2). Export values for most livestock and livestock products are forecast to fall due to lower export prices outweighing higher export volumes. This reflects global supply rising faster than global demand.

The fall in export values is driven by a decrease in sheep meat and live sheep (down 7pc to $4.2 billion), wool (down 12% to $3.0 billion), and dairy (down 4pc to $3.2 billion). However, the total value of beef, veal and live cattle exports are forecast to rise (up 6pc to $12.5 billion) as increased beef production more than offsets a fall in global beef prices.

The forecast value of livestock and livestock product exports in 2023–24 is $1.1 billion higher than in the September Agricultural Commodities Report. This upwards revision has been driven by higher export volumes and relatively strong export prices.

Falling restocker demand and rising turn-off to drive down livestock prices

Average saleyard prices for cattle, sheep, and lambs are forecast to fall in 2023–24 reflecting higher turn-off rates and lower restocker demand (Figure 1.3 & Figure 1.4). The onset of both El Niño and a positive Indian Ocean Dipole (IOD) have led to drier seasonal conditions across Australia (see Seasonal Conditions for more context). These climatic drivers are forecast to cause below average rainfall and above average temperatures across Australia over 2023–24.

In 2023–24, drier conditions are expected to reduce pasture availability and increase supplementary feed prices. This is expected to reduce farm demand for livestock, raise turn-off rates, increase livestock supply in saleyards and lower saleyard prices. For further information on the factors driving the recent decline in livestock prices, see Livestock Prices.

Although there has been some favourable rainfall in drier parts of the country in recent weeks, pasture availability remains below 2022–23 levels, and fodder continues to be in demand from both livestock producers and feedlots. In southern Australia, the availability of good quality pasture remains high, reducing fodder demand. Some of these pastures are being conserved in the form of silage and hay, increasing supply and lowering prices.

The forecast for below average rainfall and above average temperatures will also increase the risk of fires in grazing areas. For example, many fires have occurred across northern Australia over recent months; the loss of paddock feed from fires in extensive rangeland grazing systems is having a localized but severe impact on producers. A widespread outbreak of fires during summer presents a downside risk to the forecast. Fires reduce feed availability and encourage higher livestock turn-off, placing downward pressure on prices.

Average cattle saleyard prices are forecast to fall to 435 cents per kilogram (carcase weight) in 2023–24, down by 34% from 662 cents per kilogram in 2022–23 (Figure 1.3). This price decrease reflects higher cattle supply in saleyards and lower restocker demand. Rising processing capacity and elevated beef export prices are expected to place some upward pressure on average saleyard prices for cattle during the first half of 2024.

Australian beef export prices are also forecast to fall, but remain elevated, as rising global beef supply – particularly from Australia and Brazil – outweighs stronger demand from China and the United States. Beef export prices are forecast to fall by less than the average Australian saleyard price as the growth in global beef supply is forecast to be less than the growth in supply of cattle to Australian saleyards.

Average saleyard prices for both lambs and sheep are forecast to fall in 2023–24 as drier seasonal conditions result in lower restocker demand and increased turn-off rates (Figure 1.4):

- Lamb saleyard prices are forecast to fall to 540 cents per kilogram (carcase weight) in 2023–24, down by 26% from 730 cents per kilogram in 2022–23. Saleyard prices for restocker lambs are expected to fall as drier seasonal conditions reduce restocker demand. A large supply of lambs is also expected due to several years of robust flock growth and strong lambing rates.

- Sheep saleyard prices are forecast to fall to 235 cents per kilogram (carcase weight) in 2023–24, down by 43% from 415 cents per kilogram in 2022–23. The supply of sheep available for slaughter is expected to increase following several years of flock growth. Drier conditions will incentivise farmers to cull older stock and non-performing ewes.

For a more detailed analysis of the factors that are driving the decline in livestock prices, see Livestock Prices.

Australian red meat consumption expected to increase in 2023–24, total meat consumption per capita to rise

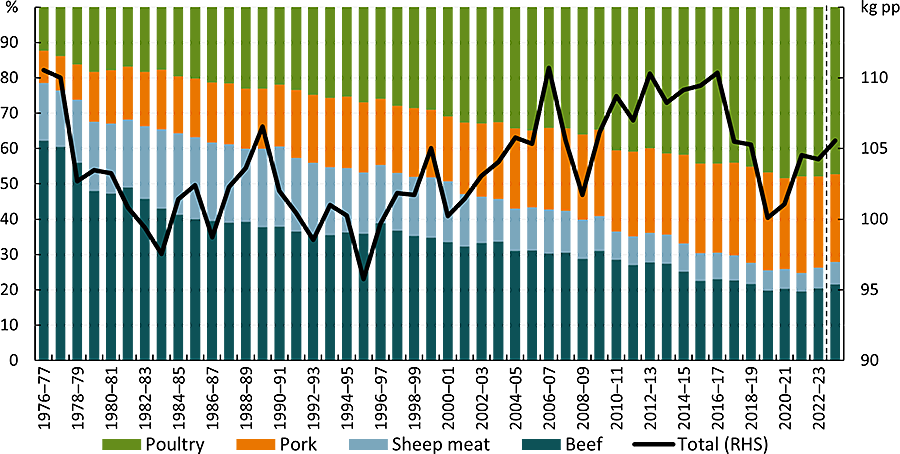

Meat per capita consumption in Australia is expected to rise in 2023–24 as lower lean meat (pork and poultry) consumption (down by 1%) is more than offset by higher red meat consumption (up by 8%) (Figure 1.5).

The composition of Australian meat consumption per capita has evolved over the past 50 years:

- Per capita meat consumption has shifted away from red meat, replaced by higher lean meat consumption (Figure 1.5). This reflects changing consumer preferences and falling lean meat prices relative to red meat which have increased affordability.

- Although consumption per capita has fallen over the past 5 years, Australia remains one of the largest per capita consumers of meat in the world, according to OECD data. Chicken meat is the most consumed meat in Australia and consumption is expected to remain relatively stable due to its affordability and consumer tastes (Figure 1.5).

Figure 1.5 Annual share of Australian meat consumption per capita by type and total meat consumption per capita

Source: ABARES; ABS

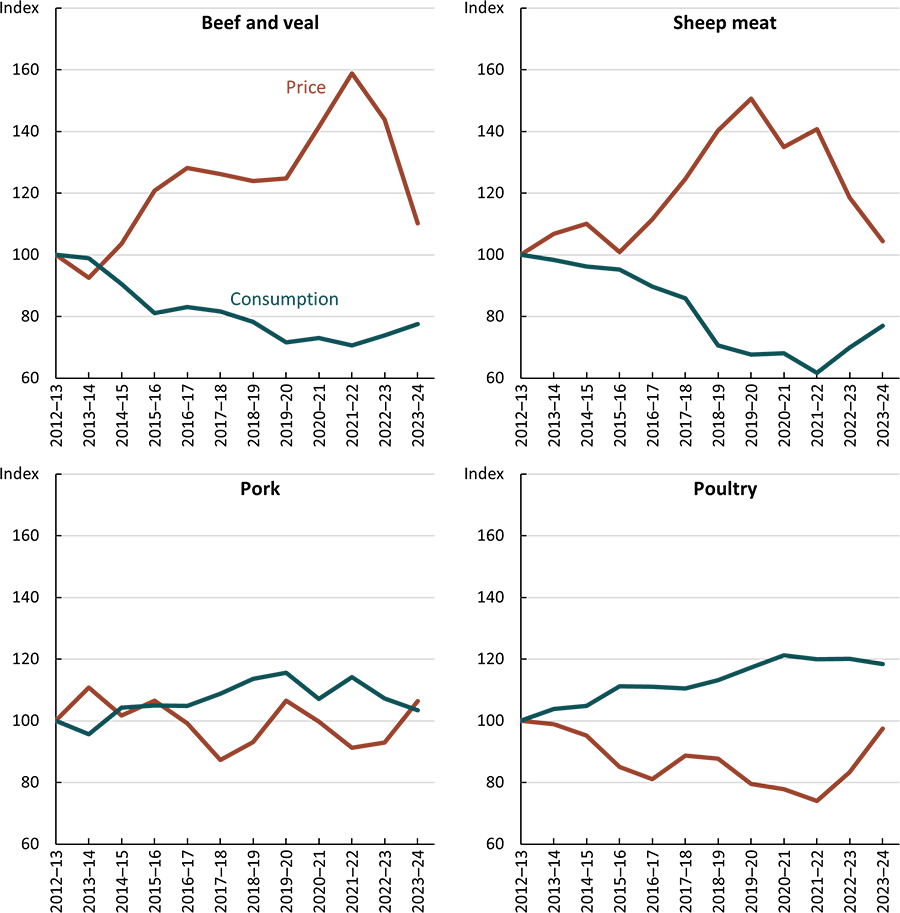

Total meat consumption per capita is forecast to rise in 2023–24. Red meat consumption is forecast to increase as changing relative prices between meat types impacts demand:

- The relative price of red meat, compared to an overall basket of meat products, is forecast to fall in 2023–24 (Figure 1.6, top two panels). Lower relative prices for red meats are expected to drive an increase in consumption per capita.

- The relative price of pork is forecast to rise which incentivises consumers to reduce pork consumption and possibly substitute towards consuming more red meats (Figure 1.6, bottom left panel).

- While the relative price of poultry is expected to rise, this is not expected to impact poultry consumption (Figure 1.6, bottom right panel). Poultry consumption per capita is expected to remain relatively stable, despite higher relative prices, due to its higher affordability and strong consumer preferences.

Figure 1.6 Annual relative price and relative consumption per capita for different meat types

Source: ABARES; ABS; MLA

HAVE YOUR SAY