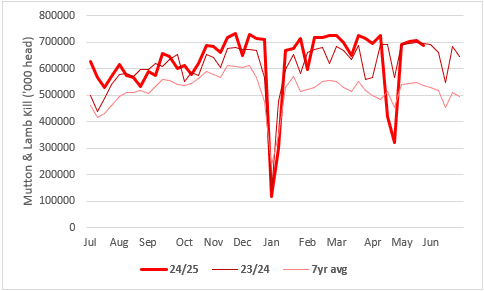

Combined lamb and mutton kill 24/25 vs 23/24 and 7yr avg. Source: MLA

Large sheep meat kills set to decline steeply through winter

The realisation that the days of heavy flock reduction and large lamb numbers are quickly coming to an end has caught the processing sector off guard and sent sheep meat prices to record levels through the past month.

The vagaries of the season meant that those who have struggled to put weight on old season lambs are now being rewarded, although most who shore lambs and fed through to autumn in the hope of better prices were disappointed. As one Elders agent pointed out, spring is the new winter, meaning that winter supply is being filled by old season lambs who have struggled to gain weight and the poor seasonal conditions — from mating through to lambing and weaning — mean that there are no new season lambs ready in spring creating a gap in supply.

Weak sheep meat prices and sustained poor seasonal conditions have seen producers cull flocks hard with one Elders agent saying amongst his clients there would be no five year-old ewes left in flocks and the 3-4 year-old ewe numbers have been culled by 20-30 percent. The result is that in some areas around 20-30pc fewer ewes may have been joined this season.

Early joined ewes (last October/November) that lambed in February/April were mostly joined in good condition and depending on the area and operator (those that supplementary fed ewes), achieved reasonable marking and weaning rates with some close to normal, but the variance in weaning rates will be quite large with ewes joined in average condition producing well below normal weaning rates.

Expect the central west of NSW and above into southern Queensland, as well as the western Riverina Hay-Ivanhoe, to be the major suppliers of the first winter sucker lambs. In the next few weeks, lambs will go onto fodder crops with the top draft of suckers being ready late August/September and the balance of lambs either being fed on depending on the spring feed situation or sold as stores to lot feeders or as light lambs for the Middle East kill (MK) trade.

Given the experience of last year, there will be a reluctance to shear lambs and feed on given the good prices available for store and light lambs and the cost and work of getting lambs to heavier weights and not being rewarded by processors.

Given the experience of last year, there will be a reluctance to shear lambs and feed on given the good prices available for store and light lambs and the cost and work of getting lambs to heavier weights and not being rewarded by processors.

Processor reluctance to offer early forward contracts has seen direct to work contract rates at $9-$10/kg cwt lag saleyard quotes $10-11/kg cwt, although some better yields achieved on hard fed lambs has meant that some returns are equivalent. By the end of June, we will see the largest proportion of contracted stock move through the system with July looking very exposed for the processor.

Welcome rain through the Riverina and Central West of NSW over the last month has improved the seasonal outlook and should allow the genuine late winter/spring lambers to avoid the very poor results that many had feared. But through the western district of Victoria and south-east South Australia there is genuine concern that weaning rates will not match marking rates as ewes running out of feed don’t seem to be mothering lambs too well.

Processors were too late in offering forward contracts to attract many takers and have exposed themselves to market forces of supply and demand with all the major export processors chasing lambs and competing with the local supermarket trade. The market is still searching for the point of resistance where processors deem lambs too expensive and withdraw from the market.

But with planned seasonal shutdowns over the next few months and talk that smaller operators will reduce shifts, processors demand is likely to ease, and rates pull back.

For mutton, multiple factors have contributed to mutton prices launching higher:

- lower numbers due to the high kills of recent years,

- producers spending money on feed to maintain core flocks rather than continuing to cull breeding stock,

- the lack of supply from Western Australia.

Talking to processors there are very few markets where sheep meat demand is inelastic (where demand is unaffected by price), in most cases Australian imported sheep meat competes with indigenous flocks and although better quality, there is a price point where it becomes too expensive.

Even in our own domestic market there will be a point where consumers will demand less at a certain price point. Interestingly our large supermarket chains have not adjusted their prices with half legs of lamb retailing for $12-15/kg which has been the case for most of the year, although this time last year when Spring lambs were available, prices were between $9-12/kg for a limited period.

Although some have enjoyed a period of prosperity in processing, talking to some processors, conditions in sheep meat processing have been increasingly difficult for the past 12 months indicating that they are having trouble passing on higher livestock prices to export customers. Processors may be prepared to absorb losses for a period (particularly larger multi species operators); however, history shows that we are close to a historical resistance point in terms of sheep meat pricing with some processors estimating their marginal breakeven cost on lamb at around $9-10/kg cw.

Also bear in mind that the major processors would be killing a lot of their own stock and using saleyards to top up kills so their average price point would be less than what they are paying in the yards. The point is don’t expect these prices rises to continue at the current pace as some processors will decide to cut back on kills to drive prices back to more sustainable levels.

US lamb prices strengthen

Since December, American demand for Australian lamb has strengthened, with prices rising moderately at around 20pc although not at the same pace as local heavy lamb values. These price rises almost mirror exactly the increase in US domestic beef values across the same period suggesting that pricing between the two may be linked.

The US currently takes around a quarter of Australia’s exported lamb, with Australia supplying nearly 80% of all imported lamb in the US, which accounts for 70% of total lamb consumption in the US.

With heavy lamb supplies likely to be challenging given the season and most having been supplementary fed and higher cost, the premiums paid for heavy export lamb suitable to the US market should widen compared to other lamb types. Given the dominance of Australian lamb in the US market, and the market segments that it occupies, the US may be one export market where Australian lamb exporters have some price influence.

Many producers have commented that if seasonal conditions don’t improve significantly they will be selling store lambs or lighter MK style lambs rather than shearing and supplementary feeding to obtain heavy trade or export weights.

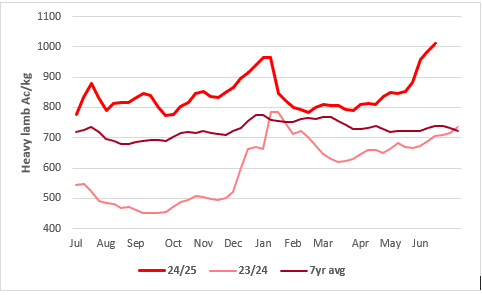

Source: MLA This chart shows the national saleyard indicators prices for heavy lambs this year vs 23/24 & 7yr avg

Don’t expect to see lamb in supermarket promotions this Spring

Local trade operators have been forced to compete with exporters to obtain heavy trade lamb supplies as supplies start to tighten heading into winter. The lack of forage crops and tough Spring and autumn seasonal conditions have seen lambs marketed sooner than normal, creating a gap in supply before the arrival of new season lambs.

Supermarket lamb prices have not moved with the livestock price indicating that supermarkets could be price averaging the meat shelf or using lamb as a lost leader. From the feedback from Elders agents, it’s unlikely that there will be an abundant supply of Spring lambs that supermarkets regularly feature in their promotions which could see promotions shift to other protein sources.

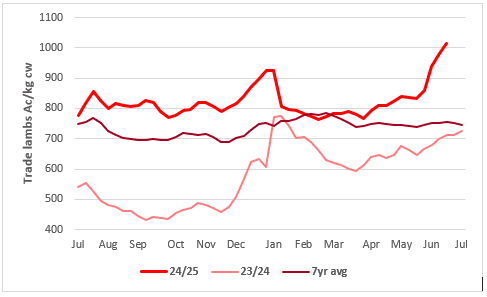

Source: MLA

This chart shows the national saleyard indicators prices for trade lambs this year vs 2023/24 & seven year average

Lower New Zealand supplies could force China to import more Aussie lamb

With the New Zealand lamb supply season widening down, China could start to turn to increased imports of Australian lamb that have already risen 12.5pc for the year to help offset the decline witnessed across the Middle East (down 20pc ytd). Australia and New Zealand share the Chinese imported sheep meat market and compete with the Chinese domestic flock which is the largest in the world.

As land use changes in New Zealand, Australia has been increasing its share of the Chinese market, which like the Middle East market is sensitive to price. Exports to the Middle East year to date have fallen by 20% which is largely price driven.

Higher Chinese demand would be needed to sustain light lamb values at current levels, particularly with talk that local lamb producers are likely to offload lambs at lighter weights rather than risk the cost of supplementary feeding in the hope of heavy lamb premiums.

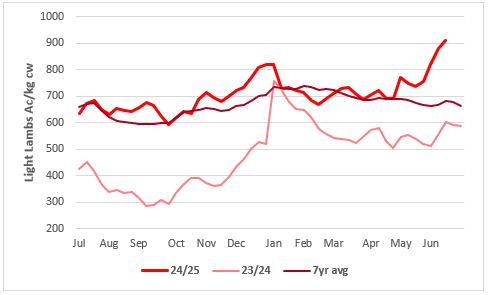

Source: MLA

This chart shows the national saleyard indicators prices for light lambs this year vs 23/24 & 7yr avg

Lambing feeding to support restockers

One of the positives from the past two difficult seasons has been the emergence of a dedicated lamb feedlot industry. Access to relatively cheap barley and store lambs has provided a strong feeding margin and the development off on-farm infrastructure to support lamb lotfeeding.

Having developed experience and working how it fits into the whole farm management program, some producers will now incorporate it into their businesses as a means of diversifying income streams, lifting productivity and adding value to grain and fodder.

Lamb feedlots should provide good competition on store lambs against restockers looking to rebuild flocks. Expect to see good supplies of store lambs this Spring with many producers unwilling to get caught feeding lambs again if the Spring fails.

Source: MLA

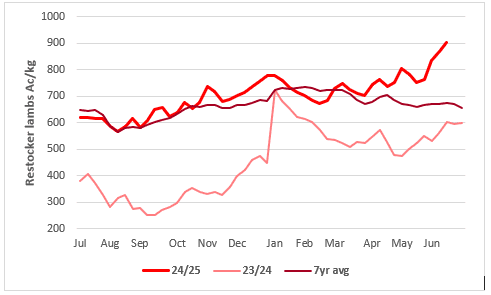

This chart shows the national saleyard indicators prices for restocker lambs this year vs 2023/24 & seven year average

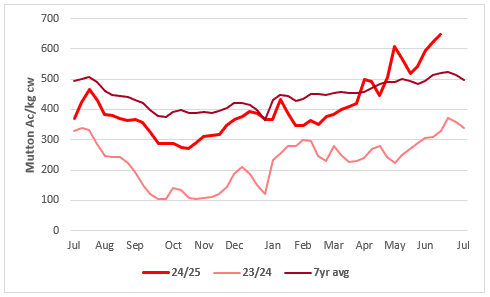

Where’s the mutton?

With any run in the seasons, it’s difficult to see mutton supplies at anywhere near the levels of the last two years. Sheep flocks have been culled hard and are now very young with only the best progeny retained. The improved season in WA, plus the hard cull over the past few years will mean that there will be far less WA sheep available to eastern states processors. Apart from some dry ewe culls after late autumn lambing, sheep supplies should dramatically tighten. Prices are currently close to reaching their historical resistance point at around $6-7/kg cwt.

Source: MLA

This chart shows the national saleyard indicators prices for mutton this year vs 2023/24 & seven year average

HAVE YOUR SAY