Richard Koch

Markets commentary by Elders economist Richard Koch

IN CONTRAST with the cattle market, prices across the sheep and lamb complex this month have been relatively stable as the industry navigates its way through tight supplies and disruptions to key export markets in the Middle East.

Lamb values have ranged from $10.50-11.50/kg dressed weight with mutton $7.50-8.50/kg for most of the year. Processor demand adjusted as prices moved out of these price brackets, to keep values mostly stable as traditionally high levels through autumn.

For the 2026 year to date, lamb and mutton kills have been down 14pc and 34pc respectively, with the declines in production slightly lower due to a lift in carcase weights due to an improved season and a rise in lamb lotfeeding that is helping to turnoff lambs at heavier weights.

Ironically, despite much weaker kill levels in comparison to recent years, Elders agents are reporting trouble obtaining kill space, with processors concentrating on working lamb supplies contracted earlier in the year. The top contract rates of around $12.50/kg are close to or above the best saleyard results.

Growth in lamb feeding sees export lambs outweigh trade numbers

The other unique quirk to this season is that there is an abundant supply of heavy lambs and limited supplies of light and trade weights. This has resulted in these categories obtaining premiums, which is unusual, particularly through winter and after the peak US demand season.

Solid feedlot and restocker interest have keep store lamb prices firm for much of the year.

In terms of export performance for the year so far, although overall lamb export volumes are down 11pc, Australia has increased the proportion of exports going to higher value markets in the United States by 2pc, China 4pc and United Kingdom 7pc. These three countries combined with markets in the Middle East take 85pc of all Australian sheepmeat exports.

US market holds despite higher prices

Lamb is having its moment in the US, perhaps driven by a shortage and the high price of beef, and a new generation of consumers is seeming to enjoy lamb as a red meat alternative.

The other trend that is assisting sales into US is that this market is focussed on higher value cuts out of heavy carcases – which are in good supply despite lower numbers of lambs – so the US market is the least likely to see a decline in volumes over the next quarter.

Consumers in the segments that Australian lamb targets in the US are not as sensitive to higher prices as some other export markets. US domestic lamb prices are averaging around 50 per cent higher than last year and about the same amount about the 5-year average as US domestic lamb supplies dwindle.

Popularity of Genghis Khan style BBQ restaurants keep Asian export firm

Asia has been another solid source of export growth for Australian lamb in 2026. Growth in demand from China (+pc) and Korea (+10pc) our two largest Asian markets (70pc of Australia’s lamb exports to Asia) is due to popularity of Genghis Khan style BBQ restaurants and less competition from New Zealand. Lamb is also sold in these markets in larger bulk packs which are popular amongst shoppers in warehouse-style stores for its better value for money offering and longer storage life.

In our third largest Asian lamb market, Malaysia, export volumes have held relatively steady (-3pc). Most of Malaysia’s sheepmeat imports are used in high-end and mid-tier hotels and restaurants, especially in Kuala Lumpur and consist of frozen products, with chilled lamb accounting for a relatively small volume.

Among Australian exports, 64pc of lamb were shoulder cuts, suitable for foodservice and adventurous home cooks, while 50pc of mutton were carcases, trunk meat, and trimmings.

Encouraging for lamb exporters over the next quarter, at the annual SIAL trade show in Shanghai China last month, lamb stands outperformed beef with some reporting 100 container lots sold in last week for smaller players.

Australia makes progress in UK while NZ focusses on the EU

Australian lamb is starting to get a foothold in the UK market, with consistent year-on-year growth aligned to improved market access (+7pc for the year to May). Australia predominantly exports lamb legs into UK retail channels.

Australia has access to a duty-free transitional quota of 41,667 carcase weight equivalent tonnes of sheepmeat into the UK in 2026 while the NZ-UK FTA came into force allowing a duty-free transitional quota of 35,000t.

New Zealand lamb has a larger footprint in retail in the EU due to more advantageous trade access. In contrast, to Australia’s duty-free quota of 5851t, the NZ-EU FTA allows NZ to export 125,769 cwe tonnes to the EU annually.

The NZ focus on lamb exports to the EU, is allowing Australia to expanding market share in the UK (under preferential access arrangements vis-à-vis NZ) but also into Asia and north America.

Middle East conflict sees a significant drop in export activity to the region

There has been a drop in lamb exports to Middle Eastern markets (-36pc) due to high cost relative to other proteins, disruptions to trade routes and higher freight costs. This has left Australian sheepmeat less competitive compared to other regional suppliers and a drop off in the tourism trade through the Middle East.

Prior to the conflict, while most of the Middle East sheepmeat market is a commodity product in carcase form, premium lamb consumption and imports have been growing, particularly in Gulf markets, driven by tourism growth, a young population and rising disposable incomes.

Excellent southern season has turned sellers into buyers through pastoral areas

The excellent season being enjoyed across large Australian southern sheepmeat regions has flipped normal seasonal supply arrangements on the head. Pastoral areas where we usually draw our numbers from this time of year.

The season is exceptional, from the northwest part from South Australia right up through to the north to the eastern side of Broken Hill and there’s a swag of stock going in there which is supporting store lambs and mutton markets as graziers there look to rebuild numbers.

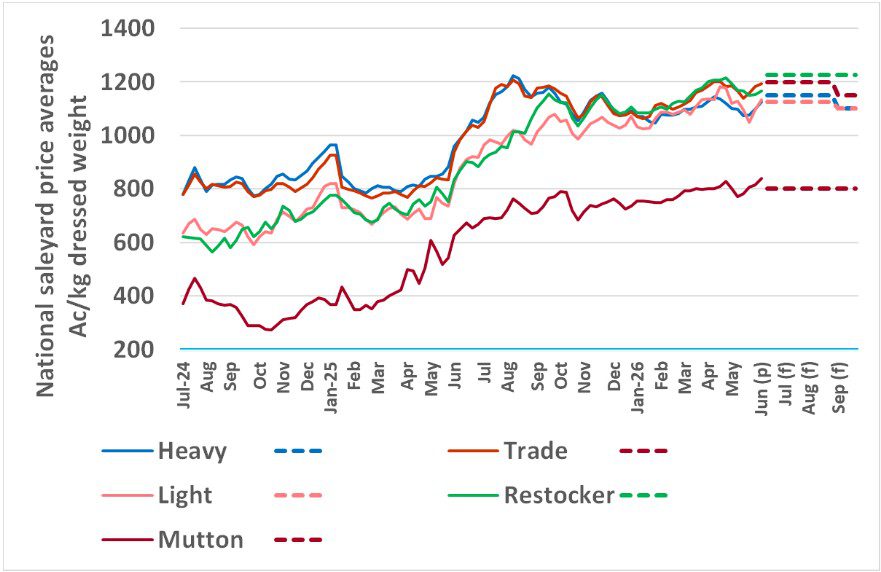

Due to firm demand from each segment of the sheepmeat industry, prices for lambs matched lofty price forecasts for the autumn season. The table below shows Australian Saleyard Indicator Prices (Ac/kg cw) by segment. Source: Meat and Livestock Australia (MLA) and Elders forecasts and projections.

(a) Actual, (f) Forecast, (p) Projected based on sales in June so far.

Based on forward contract rates it is likely that rates will hold at around current level right through the winter.

Growth in lamb lotfeeding has added another element of demand. This, combined with restockers are keeping the processors honest with the best forward contract $12.80/kg on a trade lamb with other works in the high $11’s/kg dw.

But processors have signalled that they are only willing to buy up to a certain price point which appears to be around $12/kg and around $8/kg. If prices get above these levels, processors may respond by dropping kill rates.

The reason we have kept our forecast prices levels steady around these levels are that some processors have announced that they will wind back kills to match expected seasonal declines in stock availability.

Chart showing national saleyard price averages by category for the months July 2024 to Sept 2026 Source: MLA, Elders forecasts (f).

Part of the reason that prices across the sheep and lamb complex have been so stable is that processors have been using forward contracting and adjusting their kill rates if they are unable to secure supplies; some by dropping shifts and other by signalling that they will be closing for periods of seasonal maintenance.

The good news for processors and the lamb industry in general is that the improved seasonal conditions enjoyed in southern sheepmeat regions have meant that scanning and lambing rates have been excellent. Large parts of important lamb regions are enjoying their best autumn for years after a strong finish to last spring.

Elders agents are reporting that they have never seen so many good, healthy lambs, feasting some of the best fodder crops you will likely see. The main risk is that some southern areas have not received enough runoff rain to replenish on farm water storages.

While lamb availability will remain constrained somewhat by the heavy reduction in flock numbers over the past three years and a move to keep some ewe lambs for flocks rebuilding, it is likely that lamb supply will improve in the spring compared to last year.

Reports last week that eastern states feeders were trying to contract Western Australian store lambs at +$5/kg liveweight tells us that prices are unlikely to ease too far before the start of spring. Although there may be some of the normal seasonal spring supply pressure, it is unlikely that prices will fall off a cliff.

This is why we have kept our forecasts relatively firm through the winter months before easing moderately in September.

(a) Actual, (f) Forecast, (p) Projected based on sales in June so far. Source: MLA and Elders forecasts & projections.

HAVE YOUR SAY