StoneX Australian meats and livestock manager Ripley Atkinson.

AUSTRALIA’S sheep flock will continue to rebuild this year and export demand will grow for lamb, according to StoneX Australian meats and livestock manager Ripley Atkinson.

At the Intercollegiate Meat Judging Competition conference in Wagga Wagga last week, Mr Atkinson said while global trade factors play a role, the biggest impact on Australia’s livestock markets is the weather, followed closely by local supply and demand factors.

Less lambs to hit the market

Sheep producers are starting to rebuild their numbers, according to Mr Atkinson, who said short mutton supply, high breeder ewe prices and weakening lamb slaughter numbers suggested this.

“I believe we will see shorter spring supply than usual this year as more producers retain both a larger share of their ewe lambs and also older mutton for another joining to rebuild their flock,” he said.

“The other thing to consider is wool prices are at seven-year highs.

“That is positive for producers rebuilding because they’re getting a clip off their ewes and are more likely to hold merino ewes back.”

While high lamb prices are good for producers, Mr Atkinson warned lambs at $12 a kilogram carcase weight were starting to test processors.

“Processors with start to cycle out of lambs and put mutton or goats through the plant instead, because of the economics,” he said.

“The economics are important to consider because they can only process lambs at $12 to $13 per kg so long.

“While it is good for producers, there has to be balance in the market where everyone makes money and at the moment processers aren’t making money on lambs.”

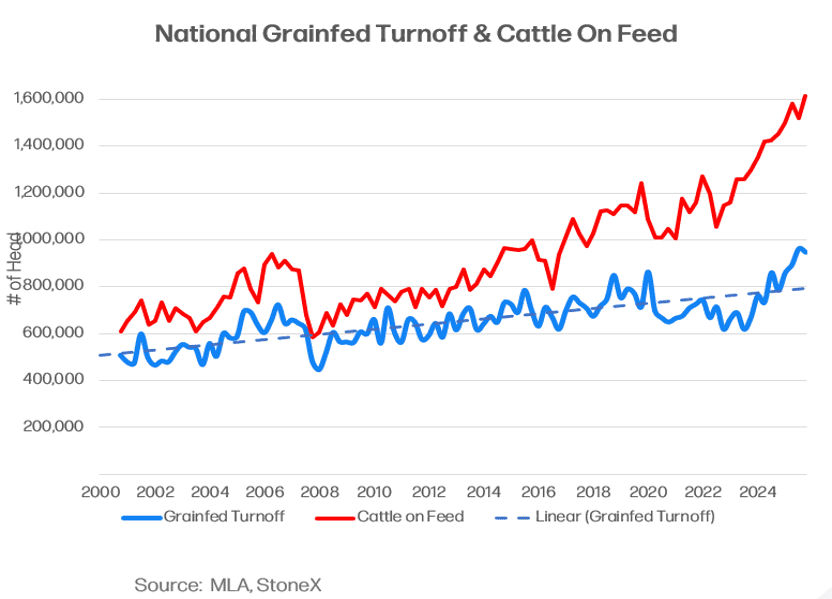

Another factor influencing the sheep industry is the rapid uptake of lotfeeding in the last 12 to 18 months.

“It has been astronomical and what it will ultimately do is remove the very significant peaks and troughs in supply of sheep, because producers will have the capacity to hold them longer and that’s something to be mindful of moving forwards,” Mr Atkinson said.

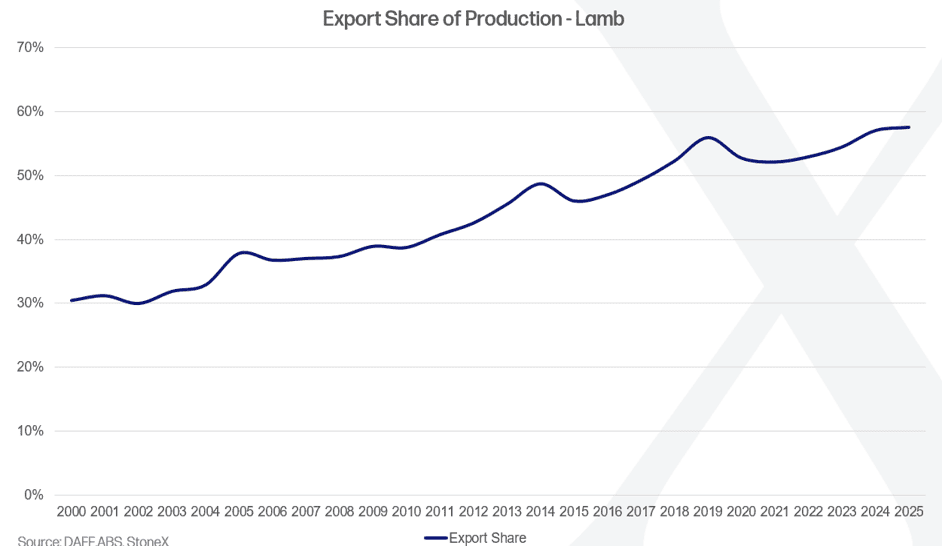

Exports now dominate lamb over domestic market

Since 2000, Australia’s lamb exports have grown from taking close to 30pc of Australia’s production to nearly 60pc and Mr Atkinson expects that will continue to increase to 80pc, in line with beef exports.

“We have hundreds of millions of people around the world, willing to pay substantially higher rates than the domestic Australian consumer,” he said.

“Exporters and processors will look to send it to the highest bidder and in the next 10, 15 years, I think it will end up like beef.

“We have seen diversification in our sheepmeat export markets. We’re seeing really positive growth in places like the UK, Taiwan, New Zealand and Canada,” Mr Atkinson said.

“That gives us really good opportunities, and we haven’t even started to see significant volumes move into India, the most populous place in the world.

“They love their sheep meat and Australia is by far the largest supplier of sheepmeat globally with the NZ lamb sector continuing to decline.”

Overall, Mr Atkinson said Australia’s sheep and lamb sector was in a really good position with a good foundation domestically and lot feeding starting to smooth out the highs and lows of supply.

“Processors have the capacity to handle the volume.

“We’ve seen in the last four years, and then we diversify their export markets,” he said.

“It leads the sheep meat sector long-term in a really healthy viable position, and probably got more growth up at an export level, diversifications for a new adaptation.”

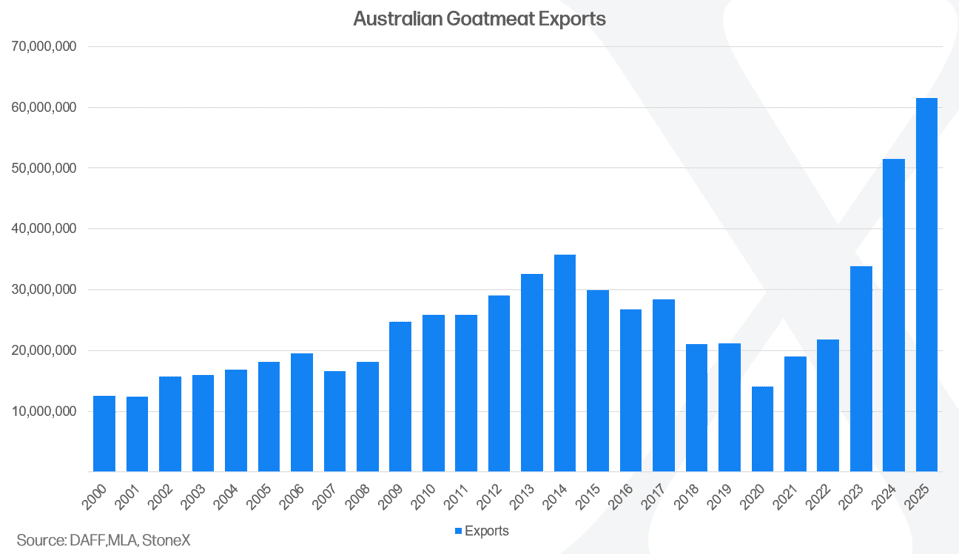

Goat production records and prices continue to lift

Mr Atkinson said the shift towards more managed goat herds has allowed a significant rebuild to happen in just three years.

“The 2025 export numbers show a record of 60,000 metric tons,” he said.

“So we have record production and record export volumes but we also have really strong prices with goat prices moving back towards five-year highs.

“That gives you an indication, much like with cattle, the supply is becoming less relevant to determine price, because the system can now handle the numbers.”

Beef cattle – a grass-driven market

Mr Atkinson explained the autumn rain in the south had allowed producers to restock and they were willing to pay at the top end for light cattle.

“For the last six to twelve months we have seen feeder prices be above restockers, but that has flipped now,” he said.

“Restockers are now operating at a premium to feeder cattle, which is the first signal of a grass driven market, producers don’t want to miss out or have grass go to waste, so they hit the restocker market.”

Herd predicted to decrease in 2026

Prior to seasonal improvements, northern New South Wales had been carrying a lot of cows, Mr Atkinson explained, and that region saw the hardest liquidation since 2019.

As a result, he predicts the herd will decrease this year because of that turnoff of cows and pregnant females.

“That will have a long-term impact on cattle supply in 2027, despite seasonal conditions improving, but we are still in a really good position,” he said.

Mr Atkison includes calves in his herd numbers which he estimated is 41.14 million head.

“The latest data shows the national adult herd has grown 6.15 per cent or 1.72 million head in 12 months,” he said.

“That growth is coming from northern Australia where our large breeder herds are and they have had a tremendous wet season.

Feeder cattle demand

Mr Atkinson predicts this is the peak period for Angus feeder cattle demand.

“We knew the supply crunch was coming at some stage on Angus feeders and the recent rains last month have really solidified that dynamic, adding to the strong upside in pricing seen recently,” he said.

“However, the Angus cattle out of northern NSW that were supposed to be sold as feeders later this year, were turned out as weaners to other regions, so the supply is still there, they have simply changed postcodes.

“For feeders on 150-200 day programs, those cattle will need to exit programs to hit the China market in early 2027 before the safeguard quota is hit again.

Another observation Mr Atkinson made was following the strong wet season in Queensland bullock numbers had grown by 510,000.

“Instead of selling them as feeders, producers have held onto them to sell as bullocks which is currently having an impact on feeder supply,” he said.

Cattle slaughter

Mr Atkinson estimates, Q2 adult cattle slaughter reached 2.57 million head, the highest quarterly rate since June 1978 which would represent a rise of 10pc or 230,000 head Year-on-Year.

(This is based off an assumption that NLRS / ABS reporting difference for Q2 was the same as Q1 2026.)

“In June 1978 carcass weights were 198kg/head, whereas Q1 2026 carcass weights were 317kg/head, which is a 119kg/head increase or 160pc,” Mr Atkinson said.

The growth in grainfed supply has helped boost carcass weights, even during dry times.

“Grainfed cattle are about 40pc of what gets processed each quarter. That has increased from about 20pc, 10 to 15 years ago,” he said.

“It has enabled us to hold carcass weights up too, so despite the south having a really tough two years, which would usually result in lighter cattle and more females being turned off, feedlots have helped keep carcass weights up.

“So that coupled with high slaughter numbers, we have had the ability to export more beef even during tough seasonal conditions.”

One of the areas to watch in processing over the next few weeks is what Victorian processors do, according to Mr Atkinson.

“We’re seeing an easing in Victorian weekly slaughter rates – we need to watch this to see if it is just a blip, or due to economics and those processors winding back kill chain speed,” he said.

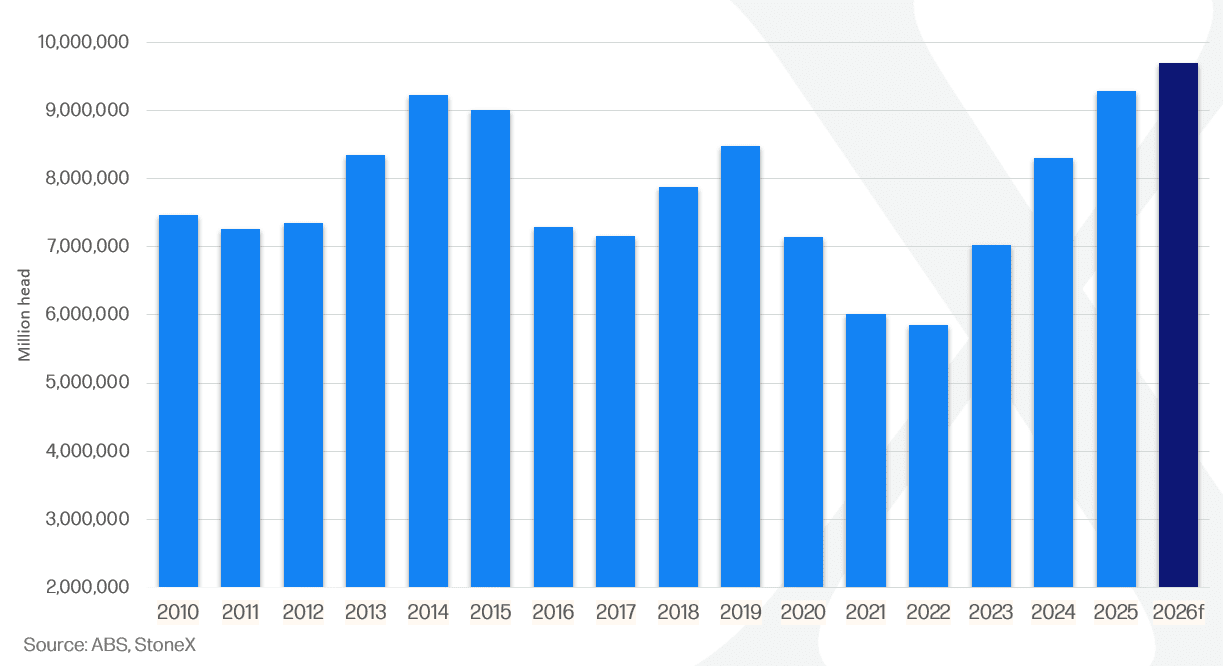

Mr Atkinson expects slaughter will hit 50-year highs at 9.7 million head this year.

Brazil as a competitor

Mr Atkinson said Australia should be paying more attention to Brazil as a market competitor.

“Currently they do 9 million head of grainfed cattle a year – if they lifted that, which they intend to, to say 50pc of their 42 million head they process per annum – we’re competing head on, likely in Japan, South Korea, China and the US with similar grain-fed product – that’s a big challenge we’re going to have to face up to,” he said.

“Last year we processed a record 3.66 million head of grainfed cattle and will likely top that again in 2026 but its only one-third of Brazil’s current grain-fed throughput, to put things into perspective.”

More immediately, Mr Atkinson explained Brazil is likely to put pressure on Australian beef in the US market this year once it hits its China quota.

“Brazil has about 500,000 to 600,000 tonnes of beef it has to put somewhere else when it hits its China quota, the US is a lot closer and can handle the volume and rates,” Mr Atkison said.

“How does Australia compete and position itself with Brazil in the US market? That is a really important one to watch this year.”

Price predictions

- Intense competition from South American producers Argentina & Brazil, coupled with some price fatigue in the US market has weighed on imported 90CL prices recently, with rates well down on the highs hit in early 2026. How this will work its way through to slaughter cattle prices in Australia will begin to become clearer as the year progresses.

- PTIC Cow & Heifer prices ‘on the box’ have reached the highest levels in at least 12 months in last week’s sale – that suggests strong demand and an early indication of producers positioning themselves for a genuine herd rebuild.

- Feeder cattle continue to lift. Crossbred prices are in the 98th percentile on record at present – whilst on a quarterly basis have increased the most in Actual terms since Argus Media began reporting that market.

Cattle outlook for second half of 2026

- Mr Atkinson predicts there will be a reduction in the cattle herd this year, not huge but a drop to 40.5 million head, driven by destocking through central eastern Australia.

- Feedlot sector to grow north of 1.75 million head on feed in 2026.

- 2026 cattle slaughter to rise slightly to the third highest level on record at 9.7 million head.

- Beef production to break 2025 record – forecast for close to 3 million metric tonne.

- Exports to break 2025 record – near 1.7 million metric tonne.

- Australian beef will move away from China and pivot towards the US where they can handle large volumes and are willing to pay.

Overall, Mr Atkinson said the outlook was positive as the current records show that the system can handle these big numbers.

“We have record numbers of cattle on feed, 50-year highs in processing numbers and cattle prices have just reached five-year highs, that gives you an indication that the system is coping with the demand and has the capacity to cope with these conditions,” he said.

This sounds frightingly like the 1920’s “Grow more Wheat Campaign”. I hope Mr Atkinson is correct, but like the years leading up to 1929 we are experiencing serious currency debasement and the outcome is unpredictable.